As the gap between new and used car prices widens, coupled with high-interest rates, buyers face a reality check.

A plurality of prospective car buyers say they prefer a new car when auto shopping, but new research shows they’re often unprepared to hand over the money to get one.

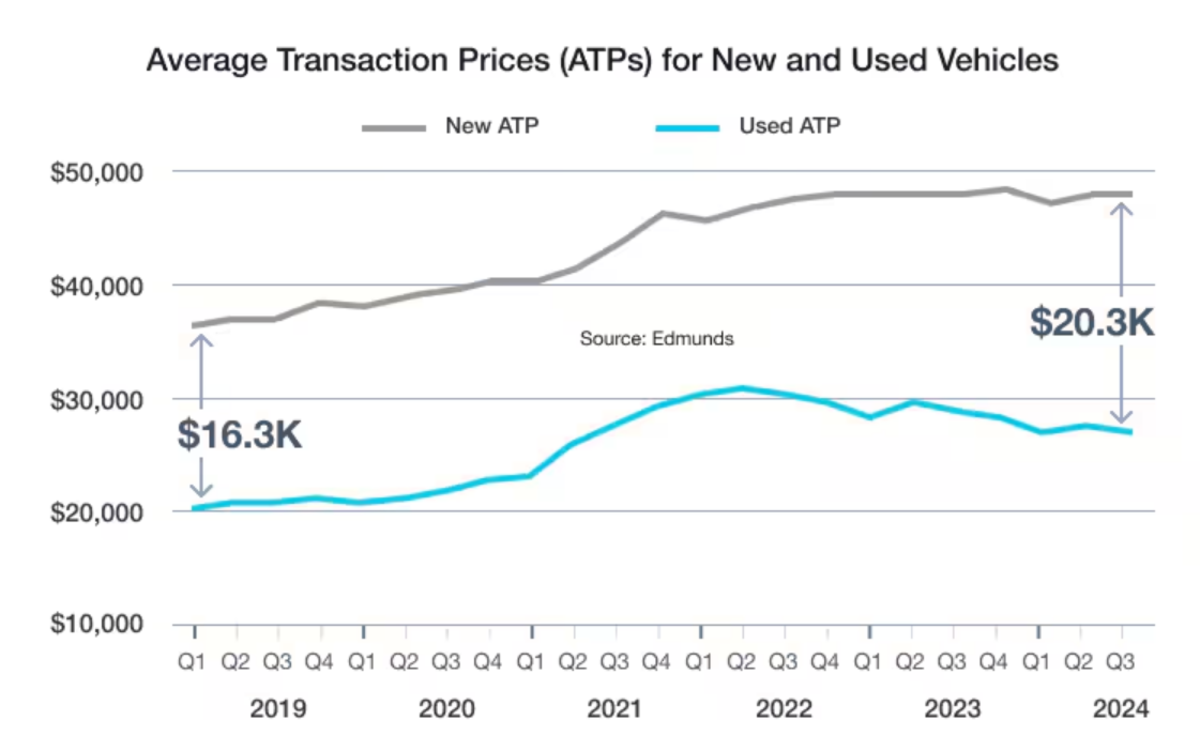

The price gap between new and used cars has reached an unprecedented level, with a $20,000 difference in average transaction prices, the largest on record, according to Edmunds. While new car prices continue to climb, the average price of a used car has declined 6.2% year over year to just over $27,000—roughly $20,000 less than the price of a new car, on average.

Despite the inflated prices in the new car market, nearly 50% of prospective buyers say they’re still more interested in buying new cars over used ones. Just over a quarter of buyers said they were more interested in a used vehicle, while less than a quarter of buyers said it “depends on the price/deal.”

New-car buyer expectations at odds with reality

Many shoppers would prefer to get behind the wheel of a new car, but that preference often butts heads with reality when faced with real-world price tags. The average price of a new vehicle hit $47,542 in Q3 2024, a price point that puts new cars out of reach for many.

This trend is particularly striking given that 14% of new-car shoppers say they want to spend $20,000 or less—a price that’s virtually nonexistent in the current new-car market, according to Edmunds. Just under half of new-car buyers surveyed said they want to spend $35,000 or less, which is more realistic but still significantly below the average new car price, meaning that options will be limited.

Modest discounts aren’t enough to lure buyers

Though discounts on new cars are beginning to return, they’re modest at best. In Q3, the average discount on a new car rose to $1,744, doubling last year’s $828 average. However, these savings barely make a dent when considering the overall high prices and interest rates. Shoppers who remember deeper incentives and zero-percent financing from pre-pandemic times may be in for a disappointment, especially as dealers face longer turnover times and are reluctant to discount further.

With new vehicles now spending an average of 57 days on dealer lots—the longest since 2021—dealers are seeing clear signs that new car prices may have surpassed what many buyers are willing or able to pay.

Used cars aren’t the deal they used to be

With the gap between new and used car prices wider than ever, over half of buyers surveyed said they’re interested in or would consider a used car depending on the deal. But even with declining prices, used cars don’t offer the same value they did before the pandemic.

Since 2019, monthly payments, down payments, and interest rates on used vehicles have all increased sharply. A significant portion of used-car buyers still expect monthly payments in the $200-$300 range, a target that today’s higher financing rates make increasingly unrealistic. For used cars, the average monthly payment now sits at $548, a sharp rise from $413 in 2019, and far above what most budget-conscious shoppers are prepared to pay.

Buyers can still find used cars in the $200-$300 monthly payment bracket, but they’re now significantly older and higher mileage compared to those purchased at similar prices just a few years ago.

Less car for more money

In 2019, a used car with a $200-300 monthly payment would require a down payment of about $2,800. For your money, you’d get a car that’s about four and a half years old with 55,000 miles. In 2024, cars in that monthly payment bracket not only require much larger down payments—just over $6,000—but they are also six and a half years old with 71,000 miles, on average.

One factor driving that change is used car loan interest rates. For our hypothetical 2024 used car, you’d be paying 10.5% interest on the car, about 2.5% higher than for a similarly priced car in 2019. This combination of inflated prices and higher interest rates has made it tougher for consumers to find desirable vehicles with affordable monthly payments even in the used market.

Final thoughts

Today’s car buyers face an uphill battle in their search for affordability. While the desire for a new car remains strong among many, the harsh reality of inflated prices and financing costs is pushing buyers toward used options. But in 2024, even used cars don’t offer the value that they used to, with buyers having to hand over more money for worse cars compared to before the pandemic.

For those on the hunt for a vehicle, a good first step is making sure your expectations align with the reality of the current market. Although the allure of a brand-new car may be tempting, shoppers may find that settling for a well-maintained used model is the most practical choice in the current market landscape.

Nicholson-Messmer, N.-M. (2024, November 7). New Car Affordability Crisis: Consumers Want New, but can’t afford it. Auto Blog. https://www.autoblog.com/news/new-car-affordability-crisis-consumers-want-new-but-cant-afford-it