The pandemic has been a global event with unprecedented impact on our industry. We learned that in these times, our customers demand convenience, efficiency, and speed in the buying process. Online transactions have become an expected part of the purchasing experience. Through it all, dealers have embraced digital tools to create a smooth car buying experience.

The latest studies showed that nearly all the car buyers in the market start their research online, regardless of how they ultimately complete their purchase.

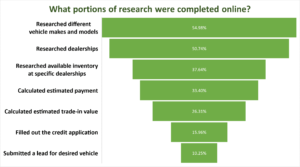

Fewer and fewer respondents completed each subsequent phase of the research process online. After submitting a lead form, the shopper either continues the process online or moves in-store.

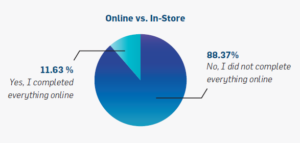

The results showed that even though some purchasers end up buying online, the majority of them visited the store to complete their transaction.

Did you complete your entire vehicle purchase online?

How you can apply this your dealership:

Online research is one of the most important parts of the car buying process. A potential buyer needs to find the right vehicle, calculate payment estimates, and even start the credit application which is an important phase while they’re shopping for cars. There’s a higher chance to complete the sale when the applicants submit an application rather than just visiting your website or calling you for further information without filling out your online application.

This only can happen if you provide them with the right amount of information and convenience as they’re engaging with your website or your online inventory.

During the “research” phase, when consumers find a car on your website that they’re interested in, calculate payment estimates, and a credit application can play an important role until they finalize their purchase with you– whether online or in-store.

UNDERSTANDING THE ONLINE BUYER

“11.63% of respondents said they completed their last vehicle purchase online. This subset of customers was asked again if they visited the dealership for any reason at all, and 77.59% still had to visit the dealership for one reason or another. Meaning of the total survey respondents, a mere 2.56% purchased 100% online. When asked about their online purchase experience, their satisfaction level was above average, with a score of 7.97 on a 10-point scale. 39% said convenience was the driving factor.”

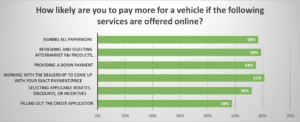

The good news is consumers are willing to pay more for their vehicle if the dealership offers the following portions of the deal online:

As the studies show, the customer needs to be able to structure their deal on your website.

Therefore, Ontario Underwriters are introducing an exciting new product to help you sell cars. We are offering our dealer partners an opportunity to add a link from their website (on other online presences such as Facebook, Kijiji, etc.)to a customized credit application. To Learn more about the product:

Reference:

REYNOLDS&REYNOLDS. (n.d.). Car buying unfolded. Reyrey.com. Retrieved April 21, 2022, from https://www.reyrey.ca/en/cp/retail-anywhere-report?utm_campaign=RR-CAN-ENG-RetailAnywhere_SY22_Q1&utm_source=RA_Car_Buying_Stats&utm_medium=CAD_Mar22