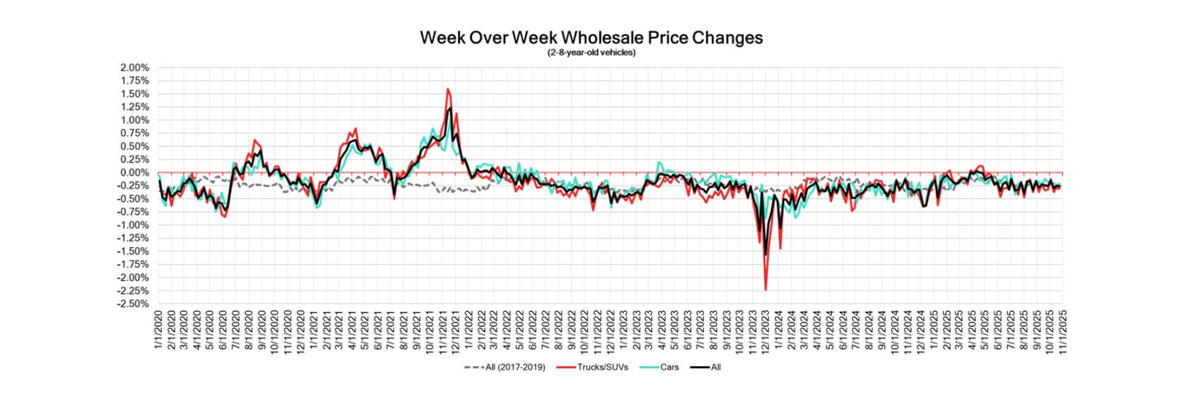

Canada’s used wholesale vehicle market posted another week of modest declines, with prices dropping -0.26 per cent for the week ending October 25 — similar to the prior week, according to Canadian Black Book. Cars fell -0.21 per cent, also similar to the previous report. And trucks and SUVs were down -0.30 per cent, which is slightly steeper than the prior week’s -0.26%.

At auction, sales rates fluctuated between 10% and 72.8%, averaging 29%, as buyers remained selective and sellers held firm on floor prices. Supply has normalized, but upstream channels continue to absorb much of the available inventory.

Retail listings showed mild softening, with the average used vehicle price sitting at $37,360, based on roughly 220,000 listings nationwide.

CBB also provided an economic snapshot, showing employment rose by 60,400 jobs (+0.3%), reversing the previous month’s losses. Retail sales are projected to dip 0.7% month-over-month.

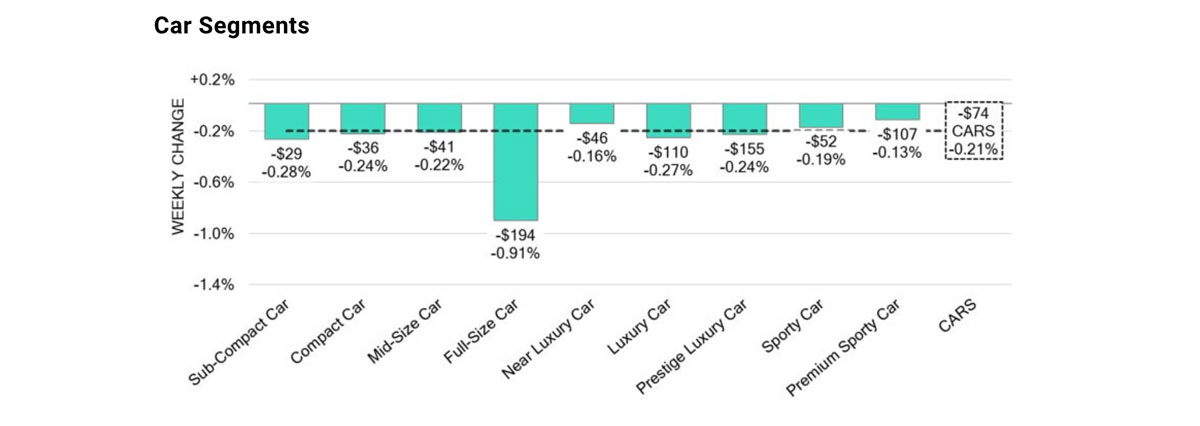

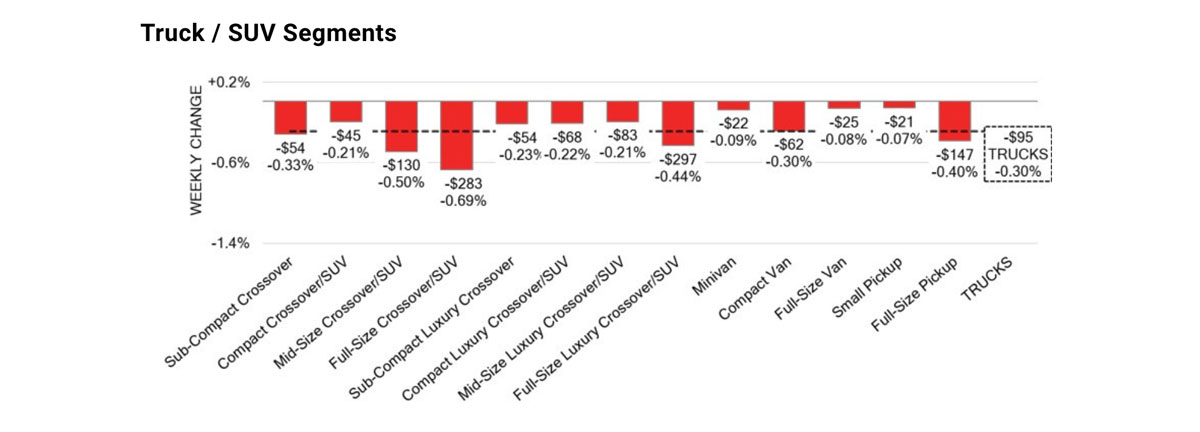

vehicle segment saw price gains. The largest declines came from full-size cars (-0.91%) and full-size crossovers/SUVs (-0.69%). Despite the decline, the rate of depreciation remains below the historical 2017-2019 average. (When comparing figures to the U.S. market, depreciation in the states accelerated: wholesale values for 2-8-year-old vehicles dropped 0.84%. CBB said it’s the sharpest decline since late 2023.)

At auction, sales rates fluctuated between 10% and 72.8%, averaging 29%, as buyers remained selective and sellers held firm on floor prices. Supply has normalized, but upstream channels continue to absorb much of the available inventory.

Retail listings showed mild softening, with the average used vehicle price sitting at $37,360, based on roughly 220,000 listings nationwide.

CBB also provided an economic snapshot, showing employment rose by 60,400 jobs (+0.3%), reversing the previous month’s losses. Retail sales are projected to dip 0.7% month-over-month.

In other news, Trump said he would end trade negotiations with Canada over a disputed Ontario ad on tariffs. Stellantis and GM’s plans to shift some vehicle production from Canada to the U.S. is being met with signals from Ottawa to reduce tariff-free import limits.

Trevor Longley, formerly of Nissan Canada, was appointed president of Stellantis Canada as Jeff Hines transitions to a new U.S. fleet role. Foreign Affairs Minister Anita Anand announced Canada now views China as a “strategic partner” amid tariff reviews on Chinese EVs.

Canadian Auto Dealer, Phillips, T., Phillips, T., dealer, C. auto, & Canadian Auto Dealer. (2025, November 5). Wholesale prices slide again as used market softens. Canadian Auto Dealer. https://canadianautodealer.ca/2025/11/wholesale-prices-slide-again-as-used-market-softens/

Dealers following Canadian used wholesale market trends may be interested to note that pricing for the week ending on August 30 has declined by -0.16%. A report from Canadian Black Book for the previous week showed a decline of -0.34%.

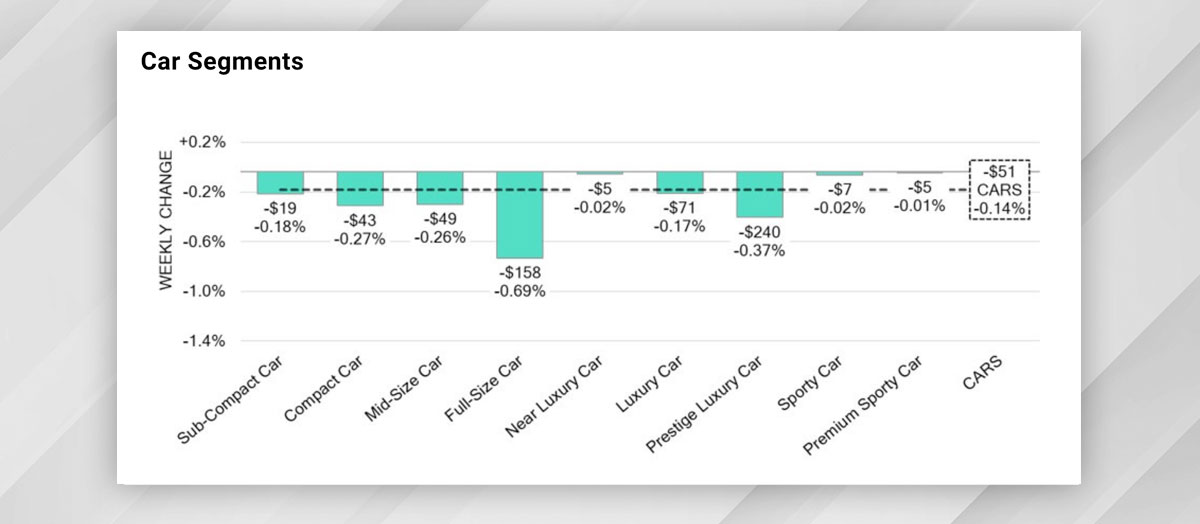

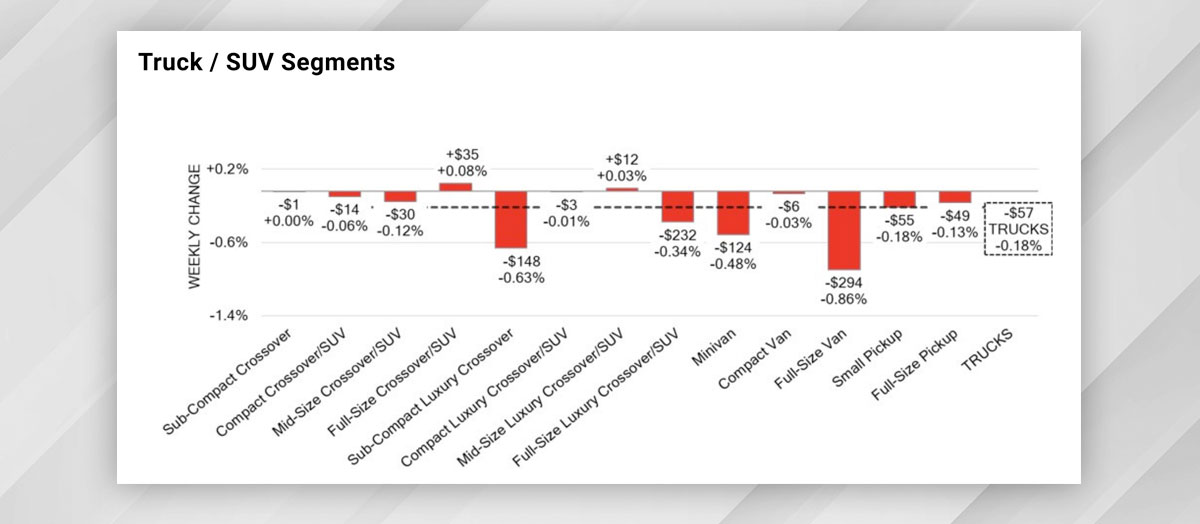

CBB’s latest Market Insights update for the current period shows car segment prices down -0.14% (compared to last week’s -0.30%), while truck/SUV segments decreased by -0.18% (versus the prior week’s -0.37%). The top positive segments are full-size crossovers/SUVs at +0.08% and mid-size luxury crossovers/SUVs at +0.03%.

“The Canadian market remains on a downward trend, with a decline less pronounced compared to previous weeks,” said CBB in its update. “Slightly more than 27% of market segments recorded an average value change exceeding ±$100. The week’s monitored auction sale rates ranged from 21.2% to 53.6%, averaging 33.4%.”

In the car segments the greatest declines came from full-size cars (-0.69%), prestige luxury cars (-0.37%), compact cars (-0.27%), and mid-size cars (-0.26%). The smallest declines were premium sports cars (-0.01%), near-luxury cars and sports cars (-0.02%).

For trucks/SUVs, the largest declines came from full-size vans (-0.86%), sub-compact luxury crossovers (-0.63%), minivans (-0.48%), and full-size luxury crossovers/SUVs (-0.34%).

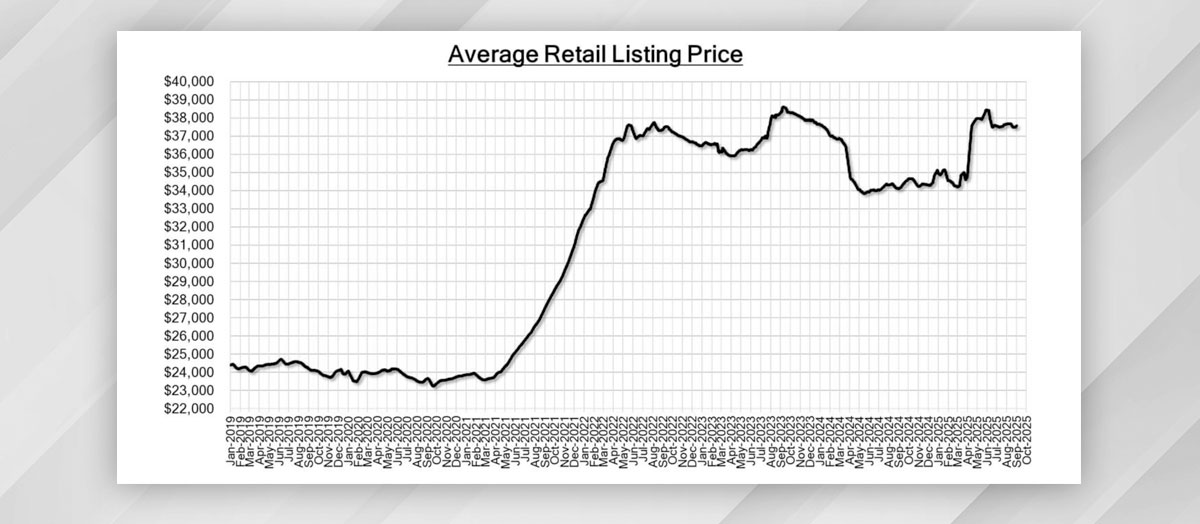

The average listing price for used vehicles is down slightly, as the 14-day moving average was at $37,600.

As for the United States, CBB said the market remained strong ahead of Labour Day, with overall values pointing to a slight decline of -0.10%. “Pickups, both full-size and small, continued their upward trend for the second consecutive week, while mid-size cars also joined the limited number of segments posting week-over-week gains.”

Phillips, T., Lefko, P., Canadian Auto Dealer, Canadian Auto Dealer, & dealer, C. auto. (2025, September 5). Used car prices down -0.16% from prior week’s -0.34%. Canadian Auto Dealer. https://canadianautodealer.ca/2025/09/used-car-prices-down-0-16-from-prior-weeks-0-34/

For all the concerns about political and economic turmoil, the first half of 2025 has been pretty good for used cars in Canada.

AutoTrader’s Q2 Price Index report shows used sales and prices were up in the second quarter and demand remained strong, building on the “pull-forward” effect that began in Q1, with car buyers acting quickly ahead of anticipated market shifts — notably tariffs.

That behavior, AutoTrader said, has driven four consecutive months of price gains, defying seasonal expectations and pushing prices above 2024 levels.

“If you’re a dealership or OEM, I think it’s a good year,” AutoTrader vice president of insights and intelligence Baris Akyurek said. “If you’re a consumer, probably not. It’s good news for dealerships because the demand is there, cars are getting sold and prices are up there, so it should be good for profitability.”

While used-car demand slipped slightly from its tariff-fueled Q1 surge, the report said, sales rose by 1.8% quarter-over-quarter and 2% since the beginning of the year. Combine those trends with tightening supply — used inventory is down 16.8% year-over-year — and the result is Canadian used prices have been rising since March, which AutoTrader said is the opposite of the typical seasonal pattern of beginning the year high and declining as the months go by.

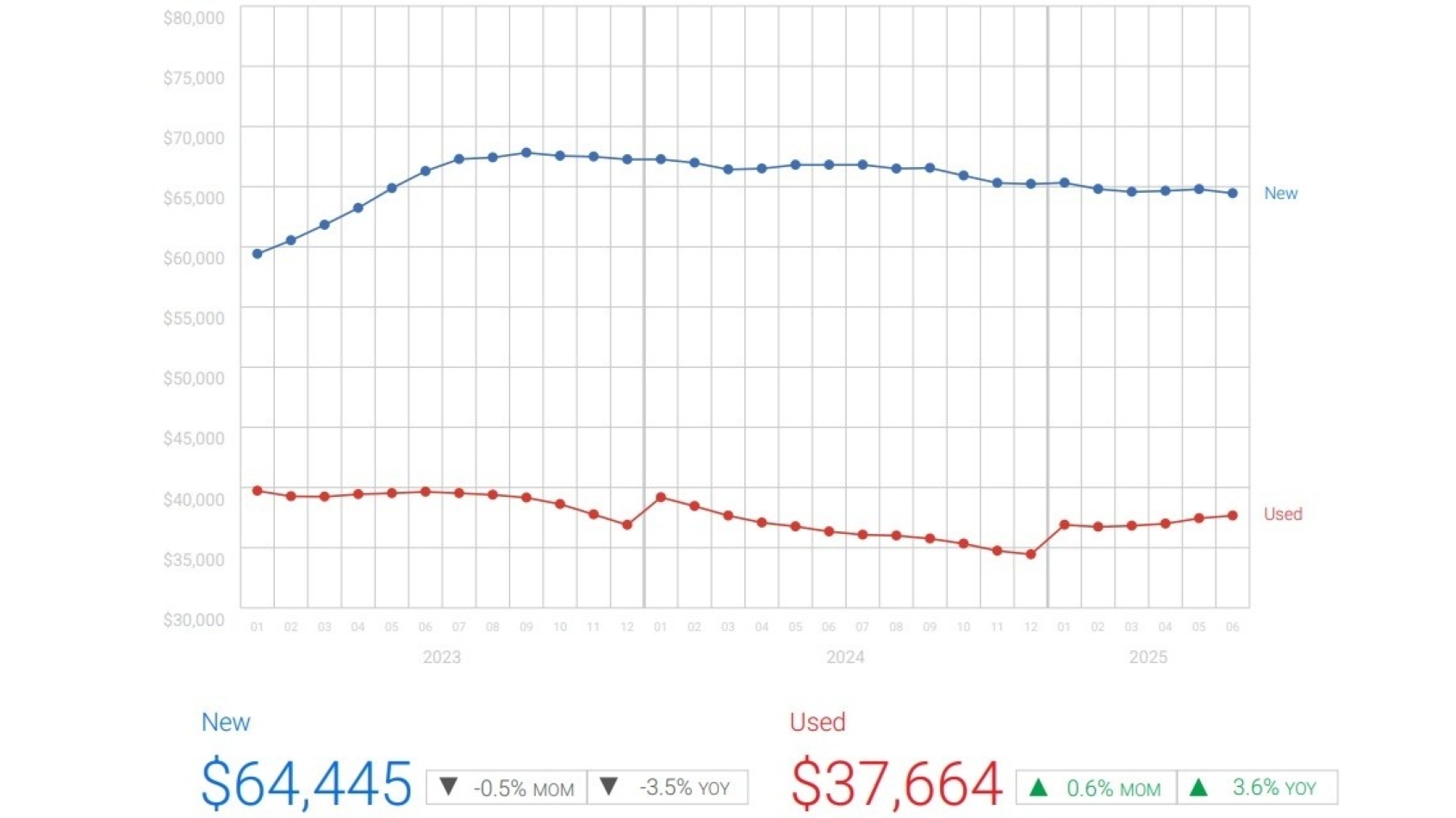

AutoTrader’s numbers showed the average price for used cars listed on its platform jumped 3.6% from Q2 2024 to $37,664, while the new-car average fell 3.5% to $64,445.

The supply shortage will continue to drive used prices up, but it actually improved — barely — in Q2, thanks to trade-ins from the pull-forward new-car sales and the reciprocal tariffs that have reduced used-vehicle exports to the U.S.

But the overall trend is still downward, AutoTrader said, as an estimated 1.5 million fewer vehicles were sold between 2020 and 2023 than originally anticipated, the effect of COVID-era production and supply chain issues, and the reduced number of lease returns.

All of that, Akyurek said, means things should look much the same in the Canadian used-vehicle market for the rest of this year.

“I have just taken my crystal ball out, and what it says is in the second half of the year, used car demand should be there,” he said. “Look, it’s been pretty strong since Q3 of last year, so the demand was there even before the tariff conversation started.

“Now there’s more demand because everybody’s been anticipating there would be an increase in prices, so consumers want to buy used cars instead of new. And in addition to all of this, given the supply crunch, the second half of the year for used markets should be pretty strong, assuming demand stays the same.”

What’s happening in the new-car market plays into that projection, too. Akyurek noted the increased new-car inventory built up before the tariffs took effect in April is now dwindling, which means new prices will likely be increasing soon, further driving used demand.

“There had been some buffer,” Akyurek said. “In the beginning, the days’ supply was sitting around 87 days, which in turn helped with the price and avoided the much anticipated price increases on the new side. But the inventory has come down a bit — the past couple of weeks it came down to 57 days, so we’re just below the quote-unquote ‘healthy’ rate of 60.

“So if things don’t change, if tariffs are still here and the inventory gets depleted, obviously it’s inevitable there’s going to be some sort of a bump in new car prices. And if that happens, there’s going to be more demand on used, period.”

The outlier when it comes to rising used-car prices is electric vehicles. The report said used battery EV prices sank to $44,077, down 7.9% year-over-year, as demand continues to soften since federal purchase incentives were paused in January and with concerns about charging infrastructure persisting.

Friedlander, A. (2025, August 12). “pull-forward” effect pulls used cars to strong performance in first half of 2025. Auto Remarketing. https://www.autoremarketing.com/arcanada/pull-forward-effect-pulls-used-cars-to-strong-performance-in-first-half-of-2025/

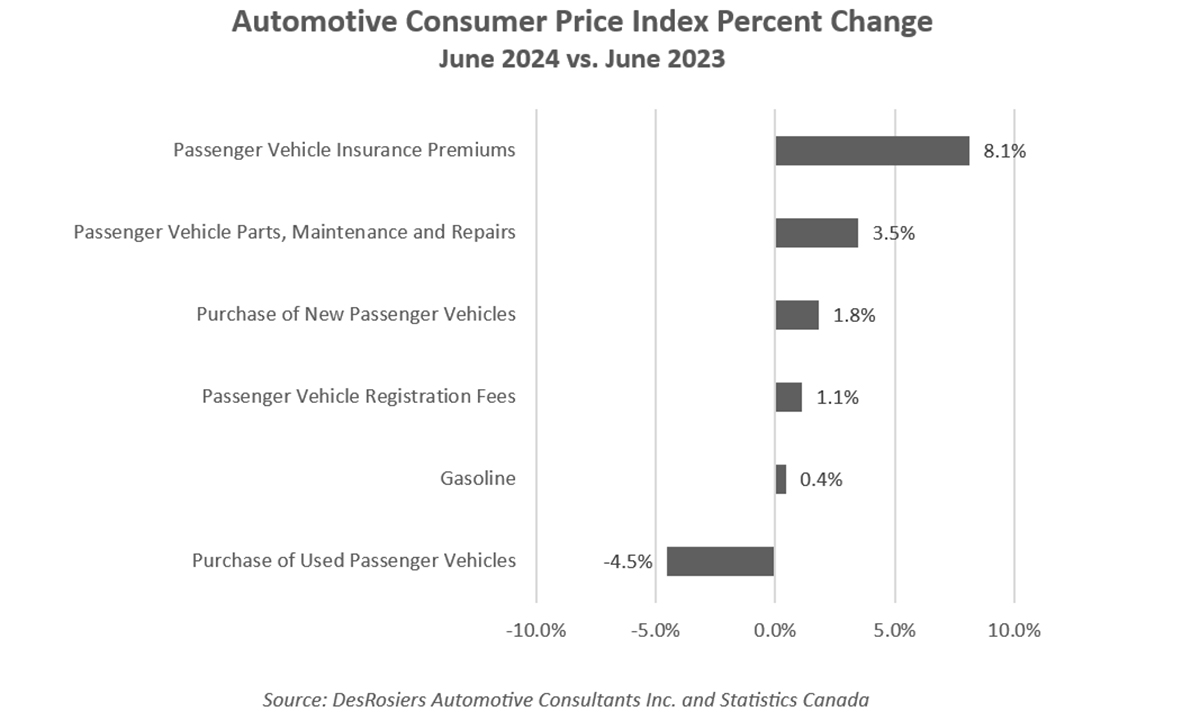

In eyeing automotive industry prices, DesRosiers Automotive Consultants has observed key areas diverging.

DAC said inflationary pressures from 2021-2023 impacted the Canadian economy — particularly the used vehicle market. But now that new vehicle supply shortages have been resolved, and the Bank of Canada started a rate cutting cycle, they say the picture has changed “dramatically.”

“It is clear that the automotive market is seeing countervailing forces at play,” said Andrew King, Managing Partner at DAC, in a statement. “The new and used markets are heading in different directions as industry dynamics reshuffle the landscape and the market works toward a new equilibrium.”

DAC said pockets of inflation remain: passenger vehicle insurance premiums rose 8.1% year-over-year in June, and passenger vehicle parts and maintenance experienced a 3.5% increase. As a category with maintenance and repair services themselves, DAC also noted a 4.2% increase — and parts CPI was up 2.9%.

On the other end, the used vehicle market, purchase prices have started to decrease — down 4.5% compared to June 2023. “This is in contrast to new vehicle CPI, which remains positive at 1.8% — supported by the twin moves toward SUVs and ZEVs,” said DAC.

Gasoline, which DAC said is acting as something of a stabilizing force, came in flat for June at 0.4%.

Canadian Auto Dealer, Canadian Auto Dealer, & dealer, C. auto. (2024, August 9). DAC sees key areas diverge in auto sector prices. Canadian Auto Dealer. https://canadianautodealer.ca/2024/08/dac-sees-key-areas-diverge-in-auto-sector-prices/

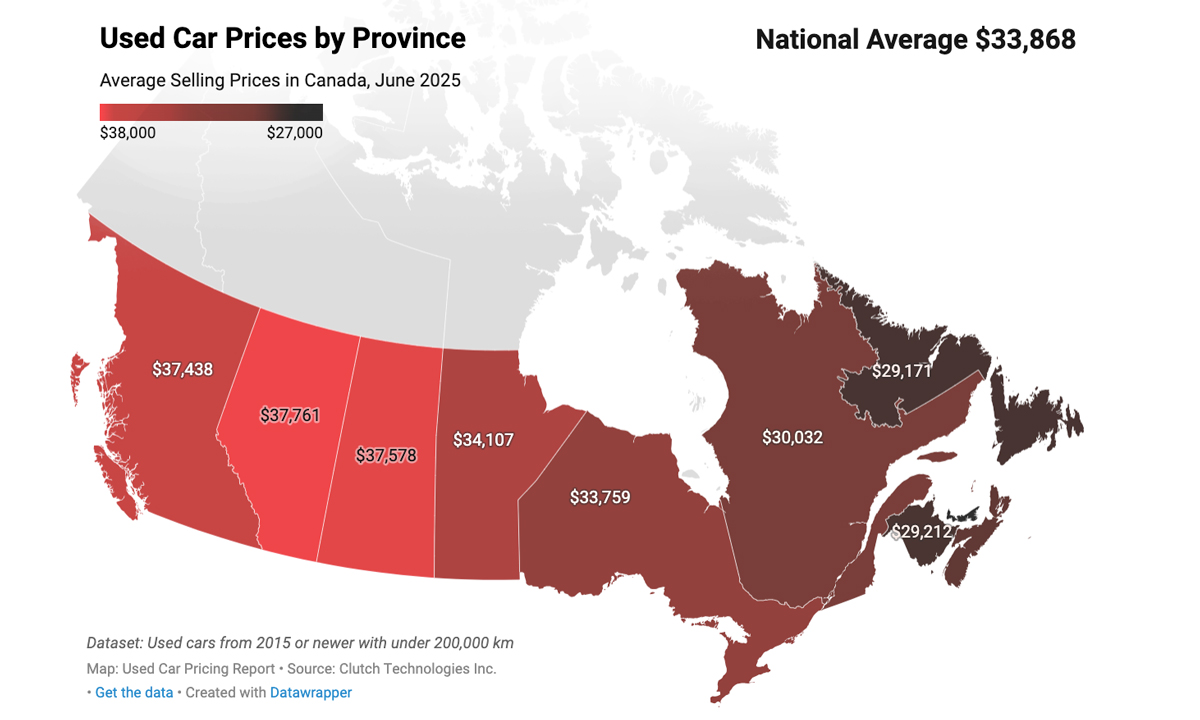

A recent report from Clutch found that used vehicle prices in Canada have once again surged, as dealers face an electric vehicle rebate deadline and the risk of increased U.S. tariffs mount.

Data from the company’s June 2025 Used Car Pricing Report shows the average used car price in Canada rose again in June to reach $33,868 — up 1.6% month-over-month and 6.3% year-over-year. Clutch said this extends the market’s streak to seven consecutive months of price increases, while also signalling a return to a high-price-floor environment.

“Several key forces combined to drive June’s increase. In Quebec — historically one of Canada’s most affordable provinces for used vehicles — the temporary suspension and relaunch of the Roulez vert EV incentive caused shoppers to temporarily step back, leading to stagnant sales volumes but a rise in average prices,” said Clutch in its report.

They said the result muted Quebec’s typical effect of pulling down the national average, thereby leaving overall Canadian prices more exposed to the higher costs typically seen in the Western provinces. Clutch also noted that hybrid vehicles are still gaining in terms of market share and average price.

The market has also remained structurally tight; with fewer lease returns and trade-ins from 2020-2023 model year vehicles, dealers face less replenishment of nearly-new inventory, “keeping broad upward pressure on prices.”

“Analysts expect the supply of desirable 2-to-4-year-old vehicles to tighten further into 2026, a direct legacy of the 2020-2023 downturn in leasing and new vehicle production,” said Clutch in its report. “That mismatch — too many older trade-ins versus not enough late-model off-leases — will continue to shape the market’s trajectory, keeping average prices elevated and reinforcing the appeal of nearly-new units despite broader economic headwinds.”

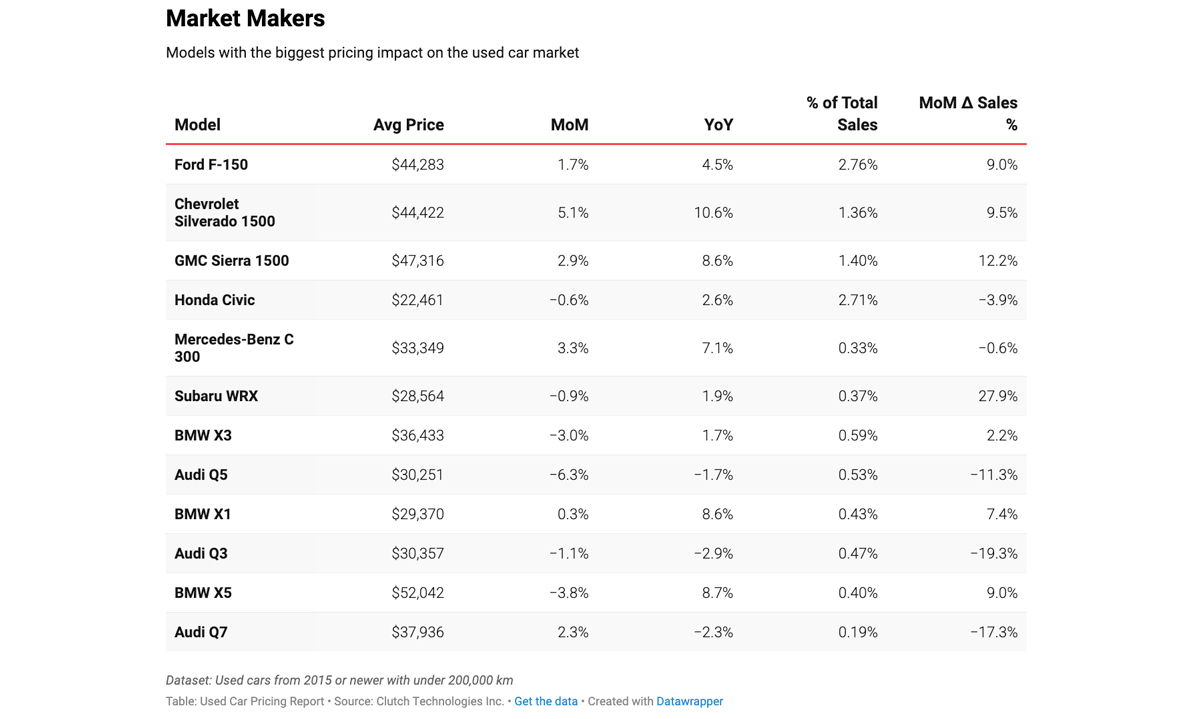

The models with the biggest pricing impact on the used car market in Canada are: the Ford F-150, Chevrolet Silverado 1500, GMC Sierra 1500, Honda Civic, Mercedes-Benz C 300, Subaru WRX, and BMW X3 — among a few others.

Lefko, P., Canadian Auto Dealer, Lefko, P., dealer, C. auto, & Canadian Auto Dealer. (2025, July 23). Canada’s used vehicle prices once again surge and why that matters. Canadian Auto Dealer. https://canadianautodealer.ca/2025/07/canadas-used-vehicle-prices-once-again-surge-and-why-that-matters/

A man looks at cars at the Mills GM dealership in Oshawa, Ont. Photo by Calgary Sun/SunMedia files

The first hints in March that United States President Donald Trump planned to impose 25 per cent tariffs on automobiles created a situation that many analysts predicted: some consumers rushed to purchase a new vehicle before the tariffs took effect. Since then, sales have continued to roll along at a brisk pace, outpacing 2024 levels — even after U.S. tariffs and Canadian counter tariffs took effect in early April — surprising many analysts, who had predicted the policies would add thousands of dollars to the cost of a vehicle and then bring a halt to sales. That hasn’t happened so far. On average, the price of a vehicle in Canada ticked up 0.9 per cent in April compared to one year earlier, according to Statistics Canada. In May, the first full month of tariffs, the average price of a vehicle ticked up 3.2 per cent. Although Statistics Canada only captures the relative price of vehicles on average, not the actual price of a vehicle, those changes are still lower than many had predicted.

The question now is whether larger price hikes lie ahead.

Matching production to demand

One of the biggest challenges tariffs pose for automakers is predicting their impact on demand and adjusting their production. Make too many cars, and an automaker finds itself with excess inventory and has to lower prices. But if an automaker produces too few vehicles, then prices could surge, which could deter some consumers from buying.“We don’t ever want to be in a position where we’re shocking the consumer and reacting,” Paul Jacobson, chief financial officer at General Motors Co., said at a conference in June. “You raise prices, you create a lull in demand and then you have to start discounting again.” He said GM anticipated the surge in demand from consumers looking to buy before the tariffs had an impact on vehicle prices.

In other words, vehicle sales may already be softening.

Tariffs implemented unevenly

The U.S. issued 25 per cent tariffs on vehicle imports on April 3. On April 9, the Canadian government issued retaliatory 25 per cent tariffs against U.S.-built vehicles, which should theoretically be causing prices to rise already.But Canada’s counter tariffs have had a negligible effect, according to an analysis released on Tuesday by DesRosiers Automotive Consultants Inc.

In the first quarter, before the counter tariffs took effect, U.S.-built vehicles accounted for 41 per cent of all new vehicle sales in Canada, but that dropped to 39 per cent in the second quarter.The Canadian counter tariffs were designed with loopholes. Five companies manufacture vehicles in Canada, and each one received a confidential “remission order,” which allows them to import an undisclosed number of vehicles from the U.S. duty-free, provided they maintain production here.A Department of Finance spokesman declined to say how many vehicles each automaker is allowed to import duty-free, and could not answer how much revenue has been raised by the duty remission scheme.But according to DesRosiers’ analysis, the number of U.S.-built vehicles sold in Canada by other manufacturers accounted for just nine per cent of new sales in the first quarter and, after the counter tariffs took effect, just seven per cent in the second quarter. “Overall, therefore, there seems to have been little change so far in vehicle sourcing,” DesRosiers said in a release.

‘Logistical gymnastics’

Vehicle prices in May only rose 3.2 per cent year over year, but that may be because consumers are only seeing the tip of the iceberg. Charles Bernard, lead economist at the Canadian Automobile Dealers Association, said that was less than what he and many of his colleagues had predicted.“I won’t complain about it,” he said. “Obviously, everyone in our industry was worried about being hit.”In part, the impact of the tariffs was mitigated because they don’t stack. Vehicles cross the border multiple times, so if a tariff was applied each time, it would quickly “spiral out of control,” he said.But both the Canadian and U.S. governments agreed that would not be wise and wrote their policies to avoid that situation. “There are reasons why we haven’t seen prices increase as much as we expected,” Bernard said. “It’s that manufacturers found ways to limit the impact.”

Some automakers stockpiled months of inventory at their dealerships so that vehicles would not be shipped across the border after the tariffs took effect. In other cases, automakers found ways to shift production between plants so that vehicles being sold in either the U.S. or Canada are built in those markets.

Automakers have also found ways to spread increased costs from tariffs across numerous different models sold throughout the world, thereby limiting the impact of the tariff on any single model. Some automakers, including Mazda Motor Corp. and Nissan Motor Co. Ltd., have stopped shipping certain models into Canada, Bernard said. “We’ve been in an environment where there’s a lot of creativity,” he said. “I call it logistical gymnastics. But the longer the situation lasts, the tougher it gets for some of these brands to find alternatives or to absorb costs. ”

Other factors beyond tariffs could affect prices

Electric-vehicle sales in Canada have been slowing. Zero-emission vehicles (ZEVs), defined broadly as battery-electric, hybrid and fuel cell vehicles, accounted for 9.7 per cent of the market in the first quarter, compared to 12.5 per cent a year ago, according to S&P Global Inc., a market data firm.

For months, auto manufacturers have railed against government policies — at the federal level as well as in provinces such as British Columbia and Quebec — that mandate that a certain percentage of their overall sales be ZEVs. Several auto industry professionals said they have pigeonholed Prime Minister Mark Carney directly during the past month, both in Ottawa and at the Calgary Stampede, to urge him to repeal the federal ZEV mandate.

The requires at least 20 per cent of the vehicles in an automaker’s 2026 model year fleet — which is what is currently being sold — be ZEVs. Current new registrations appear to be about half that amount.

As a result, some automakers say they may try to meet the target by reducing the number of internal combustion engine vehicles sold in Canada. That way, they would comply with the 20 per cent number.

“We’ve heard rumbles of companies talking to the Quebec government,” Bernard said. “Saying that with those mandates, we can’t meet the threshold, so we’re just going to send fewer cars.”

Pandemic-era challenges prepared some companies

Prime Minister Carney has set an Aug. 1 deadline to reach a trade deal with the U.S., which in theory could turn current tariffs on vehicles into a temporary measure. But one auto industry executive, who spoke on condition of anonymity, said their company is assuming that any trade deal between the U.S. and Canada will still leave some level of tariffs in place.

“I don’t think anybody expects there will be zero tariffs,” they said. “The level of aspiration on that negotiation is going to have to be managed. The U.S. president wants a baseline tariff on all jurisdictions, so we’re trying to get the best deal that we can this time.”

During the pandemic, factories in various sectors around the globe shut down in anticipation of sluggish consumer demand. Then, after consumer demand proved stronger than expected, they reopened only to face shortages of various parts that limited production.

The executive said the experience taught the auto sector about how to make its supply chain more resilient. To that end, manufacturers identified multiple sources for different parts, stockpiled certain essential inventories and found other ways to increase their agility.

Still, auto prices have substantially risen since the pandemic. Statistics Canada said the price of a new vehicle increased 22.9 per cent between June 2019 and June 2025.

AutoTrader.ca Inc., the online marketplace for new and used vehicles, said the average price of a new vehicle sold on its website in the first quarter was $65,500 compared to $40,055 in the first quarter of 2020.

Even used car prices were up 3.6 per cent in June compared to last year.

Normally, used car prices decline throughout the year, Baris Akyurek, vice-president of insights at AutoTrader.ca, said, but that hasn’t happened in 2025, which he attributes to a “pull-forward” effect in which consumers are rushing to buy vehicles before the impacts of the tariffs or other policies take hold.

Andrew King, managing partner at DesRosiers, said he thinks the impact of the tariffs will become more apparent in the second half of the year as dealerships work through inventories stockpiled before the tariffs took effect and other cost factors weigh on automakers.

The companies will continue to change their sourcing by, for example using plants outside the U.S. to bring vehicles to Canada.

“We definitely will see some price increases in the second half of the year,” he said.

Auto tariffs could still cause car prices to rise | Financial Post. (n.d.-a). https://financialpost.com/transportation/autos/auto-tariffs-could-cause-car-prices-rise

Back in December, my colleague Stephanie Wallcraft reported on the demise of new vehicles that cost less than $20,000. Decades of manufacturers’ marketing departments assuring you that you needed to be piloting your living room down the road, combined with consumers agreeing, has resulted in the crumbling of the affordable, entry-level car market. But what happens when even used car prices escalate beyond the budget of those who simply want a reliable vehicle?

New car prices being out of reach is hardly a new problem, but what do we do when even used car prices climb too high? We’re here, and it was predicted. Back during the pandemic, when shortages saw inventories depleted and no new cars coming in, Canada developed a car-shaped hole where about 1.5 million vehicles should have been. Ghost vehicles. Vehicles that would have been returned off lease or traded in…beginning in 2024. They’re not there. As tariffs threaten the health of both our auto industry and current prices, people are holding onto their vehicles longer, lending more instability to a market that is already on its back foot.

Despite reports that there are hints of a pushback by consumers against the oversized trucks and SUVs that have been so stubbornly popular, there may be little relief in sight.

Used car discussions usually focus on two different buckets: the coveted three-year-old lease returns and trade-ins that form the backbone of the used car market, and then older vehicles with a more storied life. New research from iSeeCars in the U.S. is stunning (all in USD):

“The average price of 3-year-old used cars has increased 40.9% since the pandemic, from $23,159 in 2019 to $32,635 in 2025

Used cars priced under $20,000 made up 49.3% of the 3-year-old market in 2019, compared to 11.5% of the market today

Passenger cars saw the biggest price increase since 2019, up 48.7%, with truck prices up 28.8% and SUVs up 15.4%

In 2019, 42.9% of 3-year-old Honda CR-Vs and 44.3% of Toyota RAV4s cost less than $20,000; in 2025 those numbers have dropped to almost zero.”

Used car stock and prices in Canada

Experts in Canada agree the story is the same in Canada. Baris Akyurek, vice president of insights and analysis with Auto Trader, points out the impact that the pandemic had on used car prices. “In 2019, 57.6 per cent of our used car stock was priced below $30,000. In 2025, at the end of June, that percentage sunk to 22.5 per cent.” For people hunting for an affordable vehicle, that plunge is depressing.

Auto Trader’s latest figures line up with those American numbers: The average cost of all their used inventory (as of last week) is $37,664. “Usually, we see the highest numbers in January and they decline throughout the year. This time, they’re going up, and we’re up 3.6 per cent year-over-year,” says Akyurek. Tariff threats are causing much of that tumult.

Daniel Ross, senior analyst with Canadian Black Book, agrees this American take is reflective of the Canadian situation, as well. “It’s the same scenario; cars are getting more expensive on the new side, buyers are no longer buying but keeping their current vehicles, suppressing supply. Fewer vehicles were sold in 2020-2023, so that’s also dried up the supply. We’ve seen the weighted average wholesale value increase from $20-21,000 in 2020 to $28-29,000 in 2024 (that’s roughly 38%). This has been reflected in the retail market, and with the volatility around new vehicles, the used market is feeling the pressure,” he says. Even as prices softened over the past couple of years, 2019 numbers feel like they’re on another planet.

The hunt for reasonable car prices keeps getting harder | driving. (n.d.). https://driving.ca/column/lorraine/unreasonable-car-prices-used-market

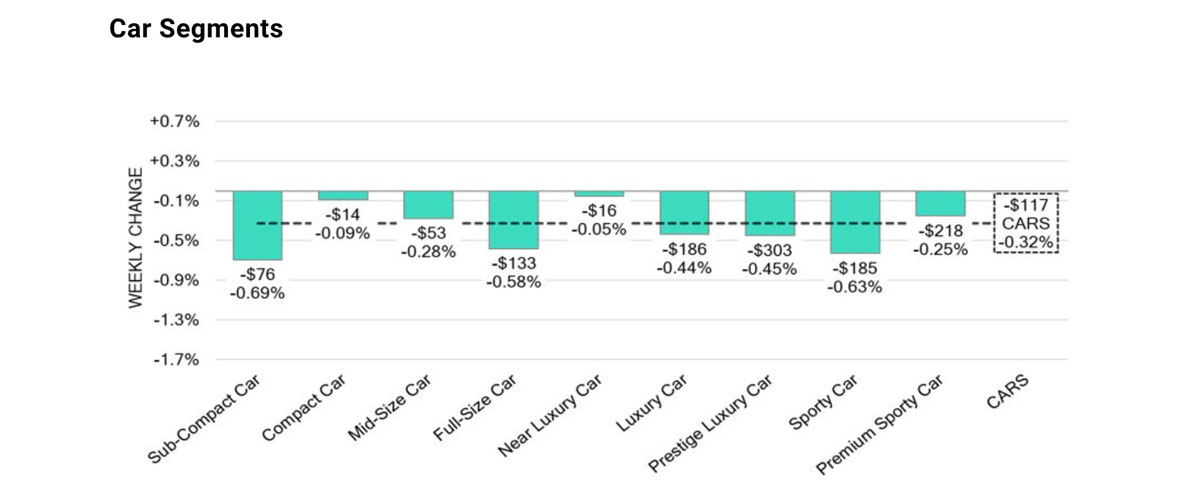

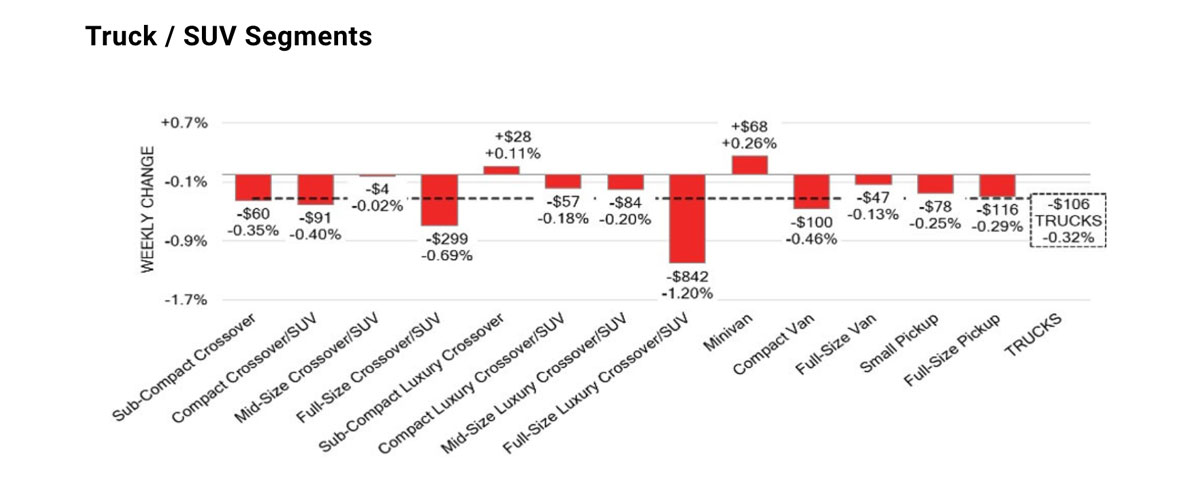

Pricing in the Canadian used wholesale market was down -0.32% for the week ending on June 28, according to Canadian Black Book. Its data report shows prices slipped lower from the prior reporting period, when pricing was -0.19%.

Both car segment prices and trucks/SUVs segment prices decreased by the same amount: -0.32%. Cars were down -0.06% the prior week, while trucks/SUVs were down -0.29%. The only positive segments overall were minivans at +0.26% and sub-compact luxury crossovers/SUVs at +0.11%.

“The Canadian market’s decrease in pricing continues with a decline more pronounced than in its previous week,” said CBB in its Market Insights report. “Just under 41% of the market segments experienced an average value change of more than ±$100.”

In the car category, the segments with the most notable declines were sub-compact cars (-0.69%), sports cars (-0.63%), and full-size cars (-0.58%). Segments with the least amount of depreciation were near-luxury cars (-0.05%) and compact cars (-0.09%).

For trucks/SUVs, the categories with the biggest decline in values were full-size luxury crossovers/SUVs (-1.20%), full-size crossovers/SUVs (-0.69%), and compact vans (-0.46%). As mentioned earlier, minivan (+0.26%) and sub-compact luxury crossovers (+0.11) were on the upside.

The average listing price for used vehicles, following the 14-day moving average, was $37,500 — based on around 220,000 used vehicles listed for sale on Canadian dealer lots.

“There has been a continuous fluctuation in sale rates across various auction lanes that can be attributed to several factors including ongoing political variances and the gradual change in floor prices,” said CBB. On supply, it said this has remained high in comparison to prior weeks; “however upstream channels continue to gain early access. There continues to be a high demand on both sides of the border for an increase in inventory and vehicles at auctions.”

Kelly, A.-M., Canadian Auto Dealer, Phillips, T., dealer, C. auto, Phillips, T., & Canadian Auto Dealer. (2025, July 2). Canadian used wholesale market prices slip -0.32%. Canadian Auto Dealer. https://canadianautodealer.ca/2025/07/canadian-used-wholesale-market-pricing-slips-to-0-32/

Despite ongoing economic uncertainty, Canadian consumers remain eager to get behind the wheel of a new or used vehicle, according to new research

Released by AutoTrader in April, the 2025 Car Shopper Perceptions & Intentions study found that 27 per cent of Canadians plan to purchase a vehicle within the next six months — a four-point increase from November 2024 and back in line with August 2024.

New vehicle purchase intentions are leading the charge, with 18 per cent of respondents eyeing a brand-new ride, up four points since late last year. This uptick in intent comes even as high interest rates and vehicle prices continue to weigh on consumer sentiment.

Confidence in the economy remains relatively low, with just 42 per cent of respondents expressing optimism. However, personal financial confidence is holding steady, with 78 per cent saying they feel secure in their own financial situation. However, that dips to 74 per cent when looking at the next six months.

Among those who have decided to delay their vehicle purchase, the top reasons include the good condition of their current vehicle (50 per cent), high vehicle prices (29 per cent) and affordability concerns (22 per cent). High interest rates were also cited by 16 per cent of respondents.

Digital tools continue to play a central role in the car-buying journey. Online automotive marketplaces are the most popular destination for used car shoppers, with 55 per cent browsing classifieds, followed by dealership websites at 39 per cent.

When it comes to completing the purchase, Canadians are increasingly open to digital options. Three in five say they would consider buying a vehicle fully online, while 88 per cent of new vehicle shoppers and 85 per cent of used vehicle shoppers prefer to complete at least part of the process digitally. Key online activities include researching vehicles, inquiring about a vehicle of interest, arranging delivery or home test drives, getting trade-in valuations, and pre-qualifying for financing.

Canadian car buyers show steady confidence despite economic pressures. Auto Service World. (2025, June 20). https://www.autoserviceworld.com/canadian-car-buyers-show-steady-confidence-despite-economic-pressures/

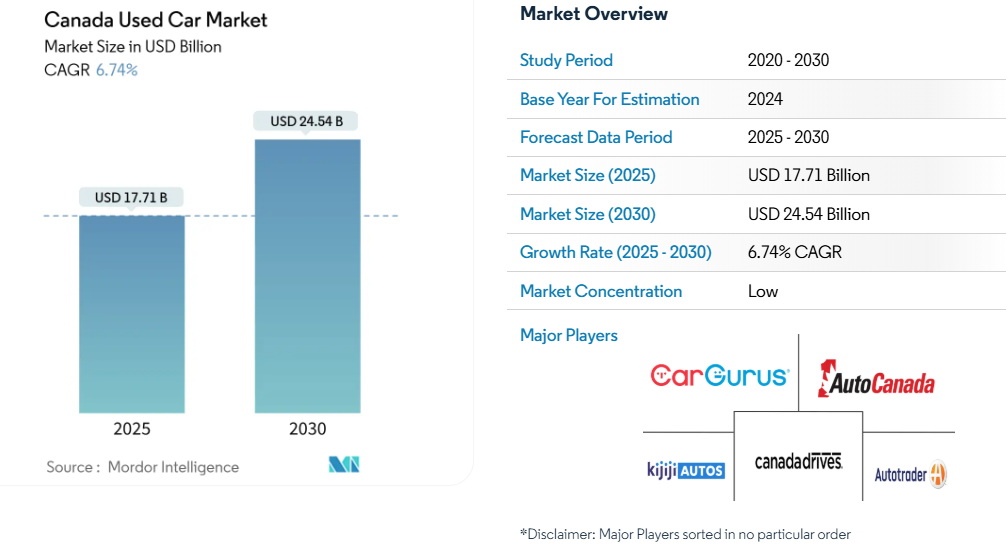

Canada Used Car Market Analysis by Mordor Intelligence

The Canadian used car market size reached USD 17.71 billion in 2025 and is forecast to climb to USD 24.54 billion by 2030, advancing at a 6.74% CAGR. Robust demand persists as consumers look for affordable mobility amid high new-vehicle prices, while digital marketplaces shorten search times and increase price transparency. Extended ownership cycles and pandemic-era production shortfalls have tightened late-model supply, elevating resale values and pushing buyers toward 3-5-year-old vehicles that balance modern features with cost savings. SUVs dominate transactions thanks to fuel-efficient powertrains and lifestyle shifts favoring cargo versatility. Online channels now originate most purchase journeys, enabling organized dealers to capture scale benefits in data-driven inventory sourcing and finance offerings. Provincial incentive stacking for low-emission vehicles, especially in Quebec and British Columbia, is accelerating used EV adoption and reshaping residual-value calculations.

Key Report Takeaways

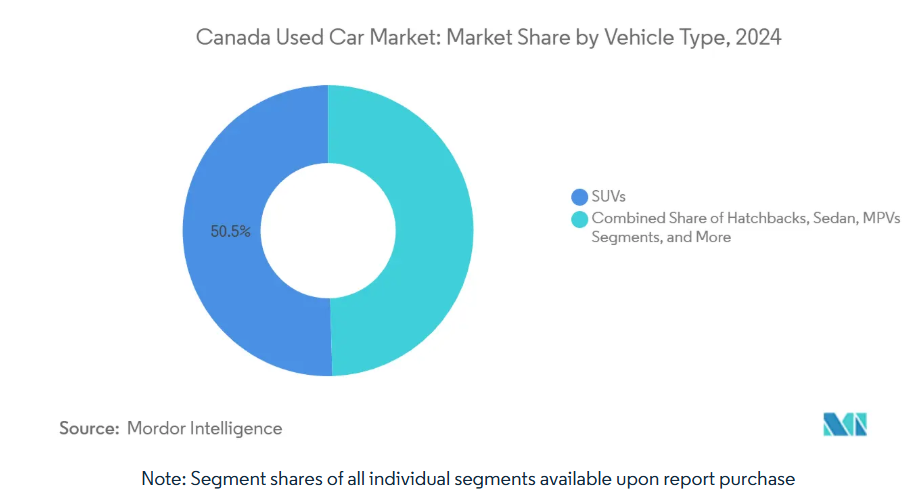

• By vehicle type, SUVs led with 50.46% of the Canadian used car market share in 2024, and expanding at a CAGR of 18.87% by 2030.

• By vehicle age, the 3–5-year segment held 38.32% share of the Canadian used car market size in 2024, while the 0–2-year segment is set to grow at 22.44% CAGR to 2030.

• By price band, the USD 10,000–14,999 bracket captured a 35.58% share in 2024, whereas Up to 30,000 is set to expand at 14.28% CAGR between 2025-2030.

• By vendor type, organized dealers commanded a 60.18% share in 2024 and are on track for a 13.77% CAGR to 2030.

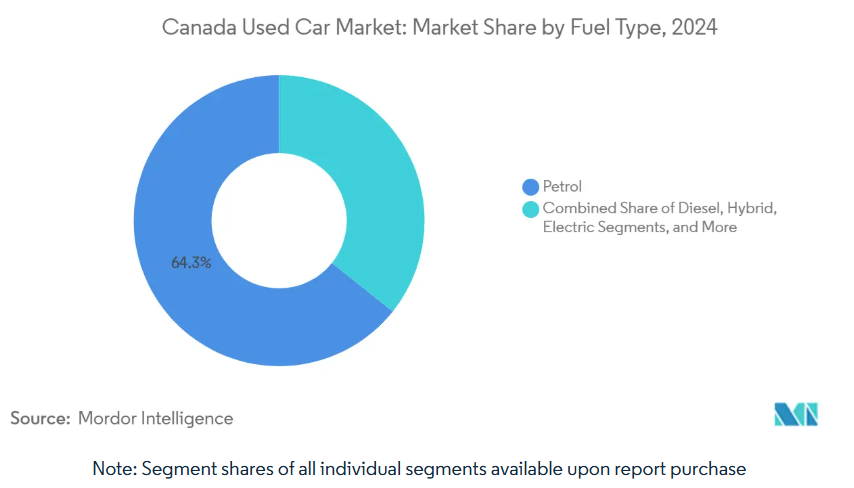

• By fuel type, petrol units represented a 64.27% share in 2024, whereas electric vehicles are poised for a 20.40% CAGR to 2030.

• By sales channel, digital classified portals accounted for 54.06% share in 2024, however online – pure-play e-Retailers is expected to grow at 25.5% CAGR by 2030.

Canada Used Car Market Trends and Insights

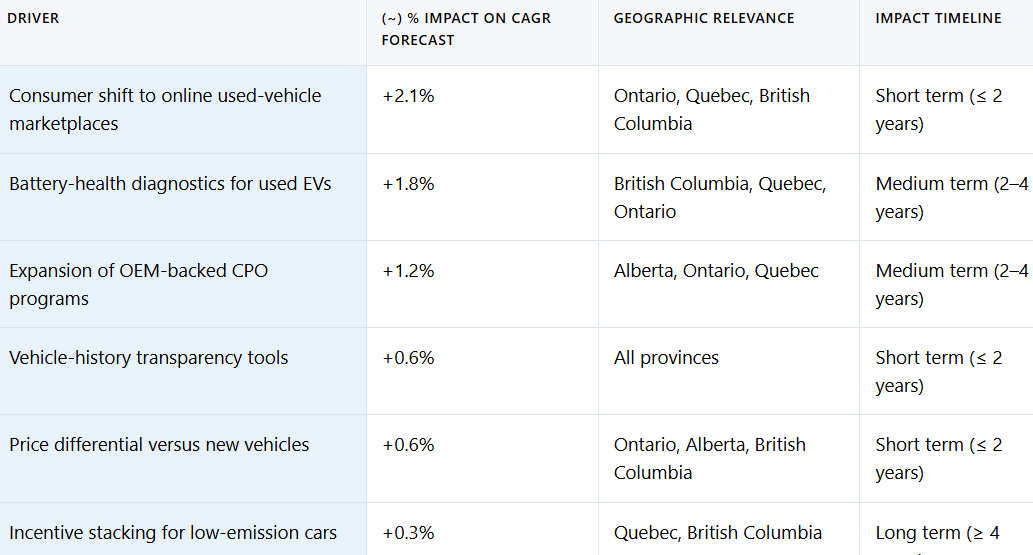

Drivers Impact Analysis

Source: Mordor Intelligence

Accelerating Consumer Shift to Online Used-Vehicle Marketplaces

More than 95% of HGregoire shoppers now begin their journey on a website before visiting a showroom, inverting the traditional research sequence. Inventory aggregation and instant price comparisons reduce search friction, and contactless delivery options resonate with post-pandemic preferences. Clutch raised USD 50 million in February 2025 to scale its home-delivery model, aiming to lower overhead and pass savings to buyers[1]“Online Used Car Seller Clutch Secures $50M Financing Round to Fund Canadian Expansion,” BNN Bloomberg, bnnbloomberg.ca. Failures such as Canada Drives, which entered creditor protection in 2023, underscore that pure-digital strategies need complementary physical infrastructure to manage inventory economics. As algorithmic pricing tools become widespread, organized vendors translate data insights into faster turn times and optimized reconditioning, widening the gap with smaller rivals.

Advanced Battery-Health Diagnostics Boosting Confidence in Used EVs

Standardized state-of-health reports quantify remaining battery capacity, directly influencing residual values and warranty underwriting. The approach tackles the 49.1% five-year depreciation typical of EVs, a steeper curve than internal-combustion cars due largely to battery uncertainty. Automakers now issue CPO warranties that specifically cover battery performance, narrowing the risk differential for second owners. Better diagnostics are expected to compress the value gap between EVs and conventional models, enlarging the addressable pool of price-sensitive shoppers. Elevated consumer trust feeds back into trade-in volumes, enriching inventory pipelines for dealers in provinces with aggressive ZEV mandates.

Expansion of OEM-Backed Certified Pre-Owned Programs

Manufacturers view certified used inventory as a retention funnel: 40% of Toyota’s CPO buyers eventually purchase a new Toyota. Tiered certification, such as Toyota’s new “silver” grade, broadens reach across budgets while maintaining inspection rigor. The scarcity of late-model vehicles lifts the strategic value of CPO schemes, enabling automakers to channel constrained supply toward the most profitable mix of new and certified units. OEMs also use CPO price floors to protect new-model transaction prices, preserving brand equity and smoothing production planning across volatile demand cycles.

Growing Availability of Vehicle-History & Inspection Transparency

CARFAX Canada’s 2024 report showed 25% of cars carry recorded damage and over 40% have active liens, intensifying the need for robust disclosure. The organization’s VIN Fraud Check flagged 127,000 potentially cloned vehicles in Ontario alone, prompting tougher penalties for inaccurate declarations. Uniform disclosure laws across major provinces have narrowed the information gap between franchised dealers and private sellers, compressing price premiums historically linked to trust. Accessible inspection apps let buyers tap third-party technicians, encouraging competitive listings and faster inventory turnover on digital portals.

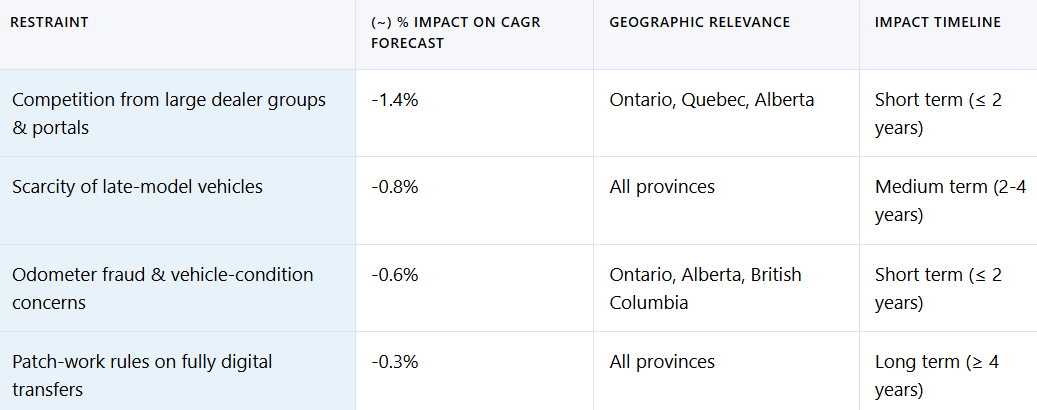

Restraints Impact Analysis

Source: Mordor Intelligence

Intensifying Competition from Large Dealer Groups & Classifieds Portals

Scale lets national chains negotiate favorable floorplan rates, run omnichannel campaigns, and deploy advanced CRM suites. AutoCanada shuttered seven under-performing RightRide sites in 2024 to concentrate capital on high-margin rooftops, illustrating portfolio optimization among majors. AutoScout24’s acquisition of TRADER Corporation folds 26 million monthly visits into a single ecosystem, layering marketplace reach atop dealer software to deepen data moats. Smaller independents must pivot toward niche inventory or hyper-local service or risk margin compression amid rising acquisition costs and digital ad inflation.

Limited Stock of Late-Model Vehicles Post-Pandemic Supply Crunch

Semiconductor shortages nearly doubled average ownership tenures, bottlenecking the flow of 0–5-year vehicles that command the steepest gross profits. Dealers expanded sourcing to consumer buy-backs, fleet disposals, and U.S. auctions, adding logistics complexity and eroding margins. Electric-vehicle scarcity is more acute as limited new-car output and strong first-owner retention yield thin secondary-market supply. Although February 2024 new-vehicle inventory reached a record 168,000 units, the lag between production recovery and used-market entry means supply tightness persists through 2027.

Segment Analysis By Vehicle Type: SUVs Drive Market Evolution

SUVs accounted for 50.46% of the Canadian used car market in 2024 and are set to advance at an 18.87% CAGR, reinforcing their role as the volume and growth engine of the Canadian used car market size. Fuel-efficiency gains and the popularity of all-wheel drive encourage households to shift away from sedans, while crossover styling appeals to city drivers seeking maneuverability.

The 0–2-year SUV cohort dominates value appreciation because of upgraded ADAS features, commanding premiums that organized dealers monetize through certified programs. Sedans retain equity in urban centers where parking constraints favor smaller footprints, yet shrinking OEM model lines put structural pressure on residuals. Hatchbacks sustain demand among first-time buyers and ride-share drivers who value low running costs. Niche categories such as convertibles and coupes rely on emotional appeal; inventory cycle times lengthen during economic slowdowns as discretionary spending softens but rebound quickly when consumer confidence returns.

Growing electrification intersects with SUV momentum as manufacturers roll out battery-electric crossovers toward 2027. Provincial incentives, most notably Quebec’s Roulez vert rebate of up to CAD 8,000 (USD 5,900), shorten payback periods and feed demand for used battery SUVs once leases mature. Dealers that invest early in high-voltage technician training capture diagnostic revenue and build customer trust[2]“About Roulez vert Program,” Government of Quebec, Quebec.ca,. However, charging-infrastructure gaps in rural Canada limit penetration, keeping petrol-powered SUVs dominant outside metropolitan corridors.

By Vehicle Age: Late-Model Premium Drives Growth

Vehicles aged 3–5 years held a 38.32% share in 2024, underlining their importance in the Canadian used car market share calculus. Buyers view this age band as the sweet spot where factory warranties overlap with significant depreciation savings. Organized dealers curate this inventory through lease-return programs that ensure consistent condition grading, allowing higher F&I attachment rates and faster turnover. In contrast, the 0–2-year bracket is slated for a 22.44% CAGR through 2030, propelled by buyers who want near-new features without absorbing first-year depreciation; its rise mirrors greater penetration of short-cycle leases in new-car financing.

Vehicles aged 6–8 years continue to satisfy budget-constrained families, though extended power-train warranties and improved corrosion protection enable owners to keep cars longer, trimming annual inflow. The 9–12-year band faces regulatory headwinds as provinces enforce stringent emissions testing, pressuring resale values and shifting such units toward export or dismantling channels. Cars older than 12 years chiefly serve cash buyers, immigrants, and credit-challenged consumers; supply is abundant but reconditioning costs and lien risk temper dealer appetite. The age profile therefore bifurcates demand between premium late-model shoppers seeking technology and lower-income buyers emphasizing price above all else.

By Price Segment: Mid-Market Concentration Reflects Affordability Pressures

The USD 10,000–14,999 range represented 35.58% of Canadian used car market transactions in 2024, anchoring affordability for middle-income households. Credit unions and captive finance arms actively court this ticket size with 60-month amortizations, balancing monthly payments against residual risk. The sub-USD 5,000 tier remains volume-rich but value-sparse; vehicles often lack modern safety features, and higher mileage inflates warranty costs for dealers, steering most activity to private sellers. Conversely, units priced above USD 30,000 are projected to rise at a 14.28% CAGR, driven by luxury-brand shoppers seeking technology packages and premium interiors without new-car obligations.

The USD 15,000–19,999 and USD 20,000–29,999 brackets benefit from widening certified-pre-owned selections, attracting buyers upgrading from older vehicles. Improved telematics and over-the-air updates extend relevance for higher-priced used models, enhancing value retention. Inflation, however, stresses discretionary budgets, prompting some consumers to trade down and reinforcing demand clustering around the sub-USD 15,000 median. As digital marketplaces publish financing calculators adjacent to listings, price sensitivity crystallizes, and sellers compete on total cost of ownership rather than sticker price alone.

By Vendor Type: Organized Dealers Gain Market Share

Organized vendors held 60.18% share in 2024, underscoring their ascendance within the Canadian used car market size. Compliance infrastructure, warranty underwriting capacity, and direct access to captive finance enable these players to outcompete informal operators. Consolidation amplifies buying power at national auctions, lowering per-unit acquisition costs while technology investments sharpen pricing models. Meanwhile, unorganized vendors—private sellers and small lots—retain lower overhead but struggle with rising regulatory complexity, including mandatory lien disclosure and odometer certification. Hybrid models are emerging, where peer-to-peer platforms bolt on professional inspection and escrow services, blurring traditional boundaries.

Organized dealers benefit disproportionately from the surge in online leads because they can integrate omnichannel touchpoints, offering click-to-door delivery and post-sale service packages that drive recurring revenue. Digital F&I add-ons such as extended warranty and GAP insurance show higher attachment rates when bundled in a single checkout flow. Independent dealers respond by specializing in subprime financing or niche inventory like performance imports. Over time, compliance costs and antifraud tech investment are expected to accelerate market share drift toward organized formats.

By Fuel Type: Electrification Reshapes Demand Patterns

Petrol vehicles made up 64.27% of transactions in 2024 and will remain the backbone of the Canadian used car market for the next five years, reflecting nationwide fueling infrastructure and resale familiarity. Yet electric vehicles are forecast to register a 20.4% CAGR through 2030, aided by overlapping federal and provincial incentives and falling battery-replacement costs. Hybrid models provide an intermediate step for households lacking home charging access, sustaining residuals in urban centers. Diesel demand declines quickly under stricter emissions rules and downtown restrictions, prompting significant value erosion in older pickups and cargo vans.

LPG/CNG conversions occupy a narrow commercial niche where fleet managers chase fuel savings over the vehicle’s remaining life. The Canadian used car industry also sees rising interest in plug-in hybrids as corporate sustainability mandates push companies to green their grey-fleet purchases. Residual-value risk for full EVs continues to hinge on battery performance; brands that publish detailed battery-health metrics during resale command price premiums. Meanwhile, dealers establish specialized reconditioning lines for high-voltage systems, opening ancillary profit streams.

By Sales Channel: Digital Transformation Accelerates

Digital classified portals recorded 54.06% share in 2024 and serve as the primary discovery point for the Canadian used car market. These sites monetize data through premium listings, financing referrals, and ancillary insurance products. Pure-play e-retailers, though still sub-scale, are expected to post a 25.5% CAGR through 2030 as logistics networks mature and consumers grow comfortable with sight-unseen purchases. OEM-certified stores seek to protect brand standards online, yet franchise agreements and limited used-inventory volumes restrain expansion pace.

Offline channels pivot to experience-centric roles, offering test drives, trade-in appraisals, and loan originations that require wet signatures in certain provinces. Digital auction platforms also gain traction among dealers, lowering transport costs by broadening national bidding pools. The rise of hybrid click-and-collect models demonstrates that most consumers still prefer a brief physical touchpoint before finalizing a high-ticket purchase, suggesting enduring relevance for brick-and-mortar assets when seamlessly integrated into online journeys.

Geography Analysis

Ontario and Quebec account for about 60% of transactions, reflecting population density, higher vehicle turnover, and robust regulatory frameworks such as OMVIC’s compulsory disclosure code. Ontario’s organized dealer penetration outpaces other regions, and its large immigrant population supports diverse vehicle mix, including compact imports. Quebec’s bilingual environment fosters local platforms like Otogo that deliver French-language interfaces and leverage provincial EV rebates to accelerate used battery-car sales. British Columbia boasts the country’s highest average used-vehicle price at CAD 41,811 (USD 30,800) because affluent buyers favor late-model SUVs and electric crossovers.

Alberta’s energy-driven economy skews demand toward pickups and large SUVs, and cyclical oil prices create pronounced swings in inventory turnover. The province’s Vehicle Odometer Rollback Program tightens compliance, reducing fraud risk and encouraging dealer investment in certification tools. Saskatchewan and Manitoba reflect smaller, price-sensitive markets where trucks dominate, and long travel distances sustain durable vehicle preferences. Atlantic Canada’s geographic isolation historically protected local dealerships, yet nationwide portals now penetrate the region, eroding legacy margins.

The federal 2035 ZEV sales mandate will magnify regional disparities in used-EV supply. Early-adopter provinces amass deeper secondary-market inventories, giving them a head start in battery-health-service ecosystems. Cross-border arbitrage remains limited because residency proof is required to claim provincial rebates, although some consumers exploit relocation loopholes. Harmonization of digital transfer protocols is progressing, but varying tax rates and lien documentation standards still complicate multi-province transactions. Over the forecast horizon, infrastructure rollout and policy alignment are expected to narrow these regional gaps.

Competitive Landscape

The top players in the Canadian used car market include AutoScout24/AutoTrader.ca, AutoCanada, HGregoire, Clutch, and CARFAX Canada. Scale allows these firms to integrate data analytics across sourcing, pricing, and F&I, producing cost advantages that smaller independents struggle to replicate. AutoScout24’s entry via TRADER acquisition unites marketplace traffic with dealer management systems, hinting at bundled software-as-a-service offerings that could lock in clients. AutoCanada continues to divest itself of under-performing rooftops to release capital for omnichannel initiatives and CPO expansion.

Technology is the primary competitive lever. CARFAX Canada’s VIN Fraud Check tool highlights the arms race in data-driven trust enhancers, compelling rivals to integrate similar antifraud layers or risk credibility loss. Clutch differentiates on home delivery and no-haggle pricing, leveraging its funding to build logistics hubs. HGregoire invests in AI-driven lead-scoring to reduce customer acquisition costs and shorten negotiation cycles. White-space opportunities persist in rural servicing, specialized EV inspection, and subprime lending, where concentration remains low.

M&A activity likely continues as global classifieds groups seek North American exposure and domestic dealers acquire specialized independents to access inventory niches. Regulatory momentum toward disclosure standardization favors well-capitalized incumbents that can absorb compliance costs, suggesting gradual consolidation but not outright dominance due to Canada’s vast geography and provincial diversity.

Recent Industry Developments

• November 2024: AutoCanada completed the sale of Okanagan Chrysler to streamline its portfolio and reduce leverage.

• September 2024: AutoCanada restructured RightRide, shuttering seven stores and shifting to an inventory-light model targeting credit-challenged buyers.

• August 2024: AutoScout24 finalized its acquisition of TRADER Corporation, bringing 26 million monthly visits under a unified platform.

Canada used car market size, share, Trends & Industry Analysis – 2030. Canada Used Car Market Size, Share, Trends & Industry Analysis – 2030. (n.d.-a). https://www.mordorintelligence.com/industry-reports/canada-used-car-market