Phillips, T., Canadian Auto Dealer, dealer, C. auto, Phillips, T., & Canadian Auto Dealer. (2025, June 4). Used vehicle market sees slight increase in pricing. Canadian Auto Dealer. https://canadianautodealer.ca/2025/06/used-vehicle-market-sees-slight-increase-in-pricing/

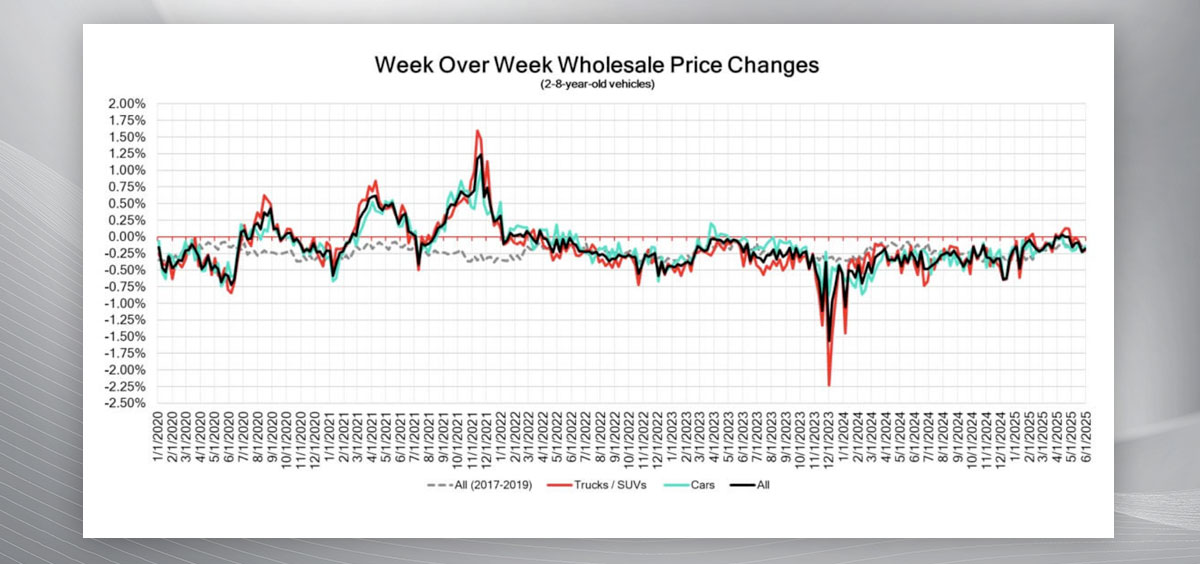

Prices are slightly up, though still down, as the Canadian used vehicle wholesale market saw a decline of -0.18% in pricing for the week ending on May 31. That’s up from the prior week’s -0.23%, though within reach — according to Canadian Black Book.

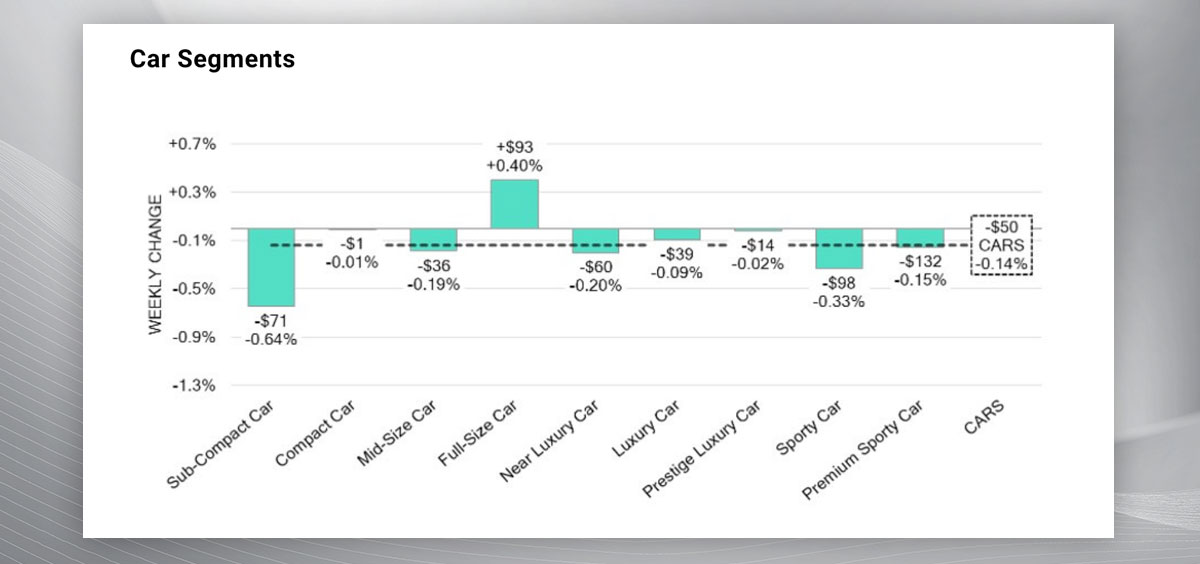

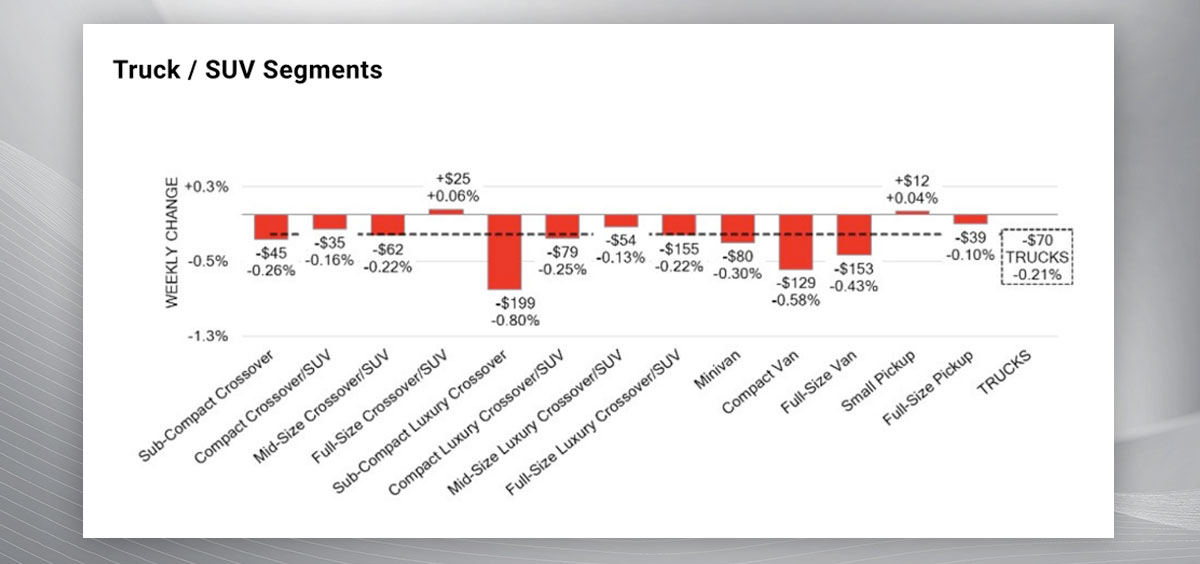

Car segment prices decreased by -0.14% (compared to -0.23 the previous week), while the truck/SUV segments were down by -0.21% (compared to -0.22 a week earlier). The largest decline in the car segments came from sub-compact cars. For trucks/SUVs, it was sub-compact luxury crossovers/SUVs.

“The Canadian market experienced a slight increase in pricing, with a decline less pronounced than in its prior week… Just under 23% of the market segments experienced an average value change of more than ±$100,” said CBB in its latest Market Update. “Supply has remained high in comparison to prior weeks; however upstream channels continue to gain early access.”

In the car category, segments with the largest depreciations included sub-compact cars (-0.64%), sports cars (-0.33%), near-luxury cars (-0.20%), and mid-size cars (-0.19%). Full-size cars experienced an increase (+0.40%).

For trucks/SUVs, segments with the largest declines were sub-compact luxury crossovers (-0.80%), compact vans (-0.58%), full-size vans (-0.43%), and minivans (-0.30%). Full-size crossovers/SUVs (+0.06%) and small pickups managed an increase (+0.04%).

The average listing price for used vehicles is slightly down; the 14-day moving average was at $38,300, based on around 220,000 used vehicles listed for sale on Canadian dealer lots.

Phillips, T., Canadian Auto Dealer, dealer, C. auto, Phillips, T., & Canadian Auto Dealer. (2025, June 4). Used vehicle market sees slight increase in pricing. Canadian Auto Dealer. https://canadianautodealer.ca/2025/06/used-vehicle-market-sees-slight-increase-in-pricing/

The average listed price for a used vehicle in Canada climbed to $37,900 at the end of April, a significant 9-percent increase from the $34,750 recorded at the beginning of that month.

These figures come from the Canadian Black Book, which uses a 14-day rolling average to track the market. According to Daniel Ross, the outlet’s senior manager of industry analysis, the surge in pricing is due to sustained demand as Canadian dealers anticipate expected price increases on new vehicles.

And those increases, of course, are the expected consequence of the U.S. auto tariffs and Canadian retaliatory measures implemented in April.

Wholesale market: Quiet but stable

Unlike the retail price surge, the wholesale market remained stable in April. Increases observed in the light truck segments were offset by decreases in passenger cars. However, Daniel Ross emphasizes that the absence of a decrease is, in itself, excellent news, in a context where the wholesale market normally depreciates weekly.

Trade war: Cascading repercussions

Growing demand for used vehicles is not a surprise. Many analysts predicted that if American tariffs were implemented, many buyers would turn away from new vehicles.

The AutoTrader.ca outlet confirms that activity in the used car market remained “very hot” throughout April.

We know that the used car market was already under pressure since the pandemic, with limited supply. The arrival of buyers deterred from new cars due to price increases risks amplifying the strain on inventory.

An AutoTrader analyst adds, “Current inventories of new vehicles are temporarily protecting Canadian consumers. But this protection is limited in time.”

Lebada Motors in Cambridge, Ontario | Photo: Lebada Motors

A short grace period

James Hamilton, managing director of the Used Car Dealers Association of Ontario, agrees. He believes that the reprieve offered by current inventories will be brief.

“Once these vehicles are sold, prepare for sticker shock on new vehicle prices.”

An increase in new car prices will create cascading pressure on the used car market, both on prices and inventory.

Exports under pressure

In recent years, around 300,000 to 400,000 Canadian used vehicles were exported to the U.S. each year — a tenth of the market, according to AutoTrader. Those exports were driven by a favourable exchange rate for Americans.

But the new tariffs—which affect both new and used vehicles—are disrupting the normal dynamic. Daniel Ross notes that American buyers have slowed their pace at Canadian auctions, adopting a more strategic approach, focusing on trucks, sports cars and luxury models.

Good news for Canadians?

A decrease in exports logically means that more used vehicles — particularly recent models from 1 to 5 years old — will remain in Canada. That could stabilize, or even reduce prices here.

The rapid price increase in April occurs within a complex and volatile commercial context. Dealers are seeking to adapt to a new tariff reality, while consumers will need to keep an eye out to avoid surprises in both the new and used car markets.

Charette, B. (2025a, May 20). Used vehicle prices rose by 9 percent in Canada in April: Car news: Auto123. auto123.com. https://www.auto123.com/en/news/used-vehicle-pricing-increased-canada-april-tariffs/72777/

Spurred by the threat of looming tariffs, we observed an active automotive market in March. AutoTrader.ca saw an uptick in user activity: visits and engagement with listings both for new and used vehicles were up substantially and car shoppers – compared with the pretariff period and same time last year – have been sending more sales inquiries to dealers and private sellers across all our platforms.

Canadian car shoppers rushed into the new car market while inventory was available and before prices could rise. And, as our research showed in early February, many used car buyers accelerated their purchases, while some new car shoppers switched to used vehicles in anticipation of price increases.

Unseasonal uptick in used car prices

Typically, what we see during ‘normal’ times, is used vehicles start with an established base price and decline throughout the year. March marks the start of the spring buying season and usually brings more buyers into the market with increased price competition. For example, in 2019 (the last ‘normal’ year), used car prices dropped 0.7 per cent in March month over month; in 2024, they were down 2.1 per cent.

This year, however, the market saw a slight uptick – a 0.3 per cent increase to $36,823 – driven by tariff-related demand and expectations of pandemic-like price surges.

More buyers entered the market and some shifted from new to used vehicles. AutoTrader has a feature that monitors price drops for vehicle listings over time and our analysis of it shows 23-per-cent fewer listings with price reductions in March alone. This trend has already continued well into April.

A silver lining for used car inventory

AutoTrader estimates 1.5 million fewer new cars were sold between 2020 and 2023, which is now affecting the used market, as those vehicles simply never entered the buy/sell pool.

The weak Canadian dollar has also led to more used vehicles being exported to the United States. An AutoTrader analysis shows a negative correlation between used car exports and the strength of the Canadian dollar: when the dollar is weak, more cars head south of the border. Now, with tariffs in place on both new and used vehicles, there’s a potential silver lining: fewer cars will be exported, allowing for more used vehicle inventory to stay in Canada. This could help ease supply constraints and relieve some pricing pressure for Canadian buyers.

New car inventory: healthy supply, for now

New car supply is relatively healthy, with 67 days’ worth of inventory (60 days is considered ‘healthy’ by industry standard). This buffer likely contributes to why new car prices have remained flat so far in 2025, though it’s not by a significant margin.

It’s also important to note that the 67-day figure is an average: some brands have more than 100 days of supply, while others have less than 30 days, so we may see more fluctuation in months to come.

What’s next?

With so much uncertainty around tariffs, it’s difficult to predict exactly what will happen next. For now, the industry outlook remains similar to what it was before tariffs. If this is a short-term disruption, the market – especially for new cars – has enough supply to absorb some volatility. However, used car supply is more challenged and demand is on the rise, which is why we’ve already seen some price movement.

Sales forecasts vary widely, so rather than wait to speculate, we suggest that if Canadian car shoppers are active in the market and have found the right vehicle, that they act promptly to secure it.

Resilience in uncertain times

As we face these recent tariffs, it’s worth remembering that the Canadian automotive market has weathered storms before. We endured the 2008 global financial crisis and navigated through the pandemic disruption earlier this decade, and adapted each time. While today’s volatility is challenging, it’s also an opportunity to learn and respond. We remain confident in our industry’s strength and resilience – and in Canadians’ determination to move forward together, no matter what the road ahead brings.

Akyurek, B. (2025, May 6). How tariffs are Shaping Canada’s automotive market so far. The Globe and Mail. https://www.theglobeandmail.com/drive/mobility/article-how-tariffs-are-shaping-canadas-automotive-market-so-far/

CARFAX Canada launched a new tool called VIN Fraud Check that alerts auto dealers if a car’s Vehicle Identification Number contains data pointing to potential fraud, or if it has been reported stolen in North America.

In a news release, the company said its new tool will now be available to dealers who access Vehicle History Reports through the CARFAX Canada dealer portal, at no additional charge. The project initiative was accelerated thanks to feedback gathered during an industry roundtable hosted by the Province of Ontario.

“By working closely with vehicle dealers, local police, and the provincial government, we’re equipping Canadian dealers with the tools they need to detect and avoid potential VIN fraud,” said Shawn Vording, President of CARFAX Canada, in a statement.

During the roundtable discussion, government representatives and industry leaders pointed to the need to address rising auto fraud by implementing the new initiatives — including data, technology, and collaboration. In a statement, Jeff Hill, Deputy Chief of Regional Operations of the Halton Regional Police Service, said technologies like VIN Fraud Check are “instrumental in helping police agencies and dealers to identify vehicles being sold fraudulently.”

“Auto theft remains a serious crime in Halton region and beyond,” he said. “It is largely driven by organized crime groups that stop at nothing to evade police detection, including VIN cloning to resell stolen vehicles for profit to fuel additional criminal activities.”

Technologies like VIN Fraud Check, he said, help remove vehicles being sold fraudulently from the pipeline and help keep Canadians safe.

Canadian Auto Dealer, dealer, C. auto, & Canadian Auto Dealer. (2025, April 24). Carfax Canada launches Vin Fraud Check Tool for dealers. Canadian Auto Dealer. https://canadianautodealer.ca/2025/04/carfax-canada-launches-vin-fraud-check-tool-for-dealers/

A car-hauler truck gasses up at a duty-free station before crossing the Ambassador Bridge into the United States at Detroit on April 1, 2025 in Windsor, Canada Photo by Bill Pugliano /Getty

The dust is starting to settle from Donald Trump’s recent tariff announcements, so this might be a good time to look at the likely impacts on the Canadian automotive sector, both in terms of manufacturing and sales. Spoiler alert: I am actually quite optimistic for Canadian car-makers and consumers.

Let’s start with a quick recap. The U.S. has applied an overall 25% tariff on Canadian goods, but has exempted, for now, most USMCA-qualifying products, including vehicles. However, light-duty vehicles are subject to a new, separate 25% tariff that is applied to all countries. The rules governing this automotive tariff provide that the applied rate of duty can be reduced by the value of the U.S. parts content in the vehicle, if that U.S. content exceeds 20% (the 20% threshold effectively eliminates non-USMCA vehicles from obtaining a lower rate of duty). By subtracting the value of U.S. parts and components in the vehicle, you lower its total value, and effectively reduce the applied rate of U.S. duty.

Canada has responded with a 25% duty of its own (often referred to as either a “surtax” or a “counter-tariff”) on U.S.-assembled vehicles. In a mirror image to the U.S., Canada will allow importers to deduct the value of any Canadian and Mexican content, effectively lowering the rate of duty on U.S.-built vehicles. For USMCA-qualifying vehicles, importers may choose to deduct the full value of the U.S. content with detailed proof of origin; or take a streamlined approach and simply claim a 15% reduction.

As a result, the effective applied rate of duty on USMCA vehicles imported from the U.S. will be 21.25%, less any further adjustment for proven U.S. content above 15%. For vehicles assembled in the U.S. that do not meet the USMCA rules, the full 25% duty would apply.

As a result, the effective applied rate of duty on USMCA vehicles imported from the U.S. will be 21.25%, less any further adjustment for proven U.S. content above 15%. For vehicles assembled in the U.S. that do not meet the USMCA rules, the full 25% duty would apply.

Workers perform vehicle assembly at the Honda of Canada Manufacturing Plant 2 in Alliston, Ontario, on April 25, 2024 Photo by Peter Power /Getty

While temporarily exempting USMCA-qualifying parts from tariffs, the U.S. does intend to apply duty to the non-U.S. content in parts. By contrast, Canada is not proposing to put duty on parts, and is in the process of establishing a duty-remission program for Canadian automakers. That program will allow companies that build cars in Canada to avoid paying the surtax on the U.S.-built vehicles they import to Canada.

So, what does all of that mean?

First of all, U.S. consumers will not be faced with a sudden 25% price increase on vehicles imported from Canada. As noted above, the dutiable value of cars imported to the U.S. can be reduced by the amount of U.S. content in the vehicle. So if, for example, 50% of the content in a Canadian-assembled vehicle is American, the vehicle’s value for duty would be reduced by half before applying the 25% tariff. That would leave the U.S. importer of the vehicle paying an effective duty rate of 12.5%. All Canadian-made vehicles incorporate U.S. content, so they will be less impacted by tariffs than imports from Europe, Japan, or Korea.

New vehicles are parked at Daikoku Pier in Yokohama, Japan on April 2, 2025 Photo by Philip Fong /Getty

Similarly, if the U.S. goes ahead with tariffs on the non-U.S. content in all imported parts, Canadian parts-makers may also enjoy a comparative advantage against their European or Asian competitors. Canadian parts often incorporate some U.S. content, too, so that will also mean lower effective rates of duty. The final form of those rules is still being worked out, but the takeaway is that, for both parts and vehicles, Canadian manufacturing operations will be better positioned to continue to do business in the U.S. than their European or Asian competitors.

Just as importantly, there will be no change to the existing competitive balance between Canada and Mexico because we are both covered by the same rules. Canada’s overall competitive position has experienced a setback, but it might not be the disaster many Canadians fear.

onsider this: previously, Canadian-assembled vehicles held a 2.5% advantage over European- or Japanese-made vehicles, thanks to the 0% rate of duty under the USMCA versus the general tariff of 2.5% on vehicles from other countries. Korean vehicles were on par with Canadian vehicles because Korea and the U.S. also had a free-trade deal.

So, returning to the scenario where a Canadian-built vehicle has 50% U.S. content, Canada’s applied-duty-rate advantage under the Trump tariffs increases from 2.5% to 12.5% against European and Japanese competitors. Against Korean-made vehicles, that advantage rises from 0% to 12.5%. Of course, U.S. content in Canadian vehicles varies by model, but our comparative advantage against all but American-made vehicles should increase under Trump’s tariffs.

Canada’s Prime Minister Mark Carney speaks at a news conference at Rideau Hall in Ottawa on March 23, 2025 Photo by Dave Chan /Getty

Canada’s decision to not follow the U.S. in applying tariffs on auto parts is also significant. Cars built in the U.S. will see increased costs because of tariffs on imported parts. Those additional costs will be baked in whether the vehicles are sold in the U.S. or exported to Canada. By contrast, since Prime Minister Carney decided to not apply tariffs on imported car parts used by vehicle assembly plants in Canada, Canadian-built cars could actually be cheaper than their American-built counterparts, which would help mitigate the tariff hit were they exported to the U.S.

That doesn’t mean there aren’t new competitive challenges for Canadian-assembled vehicles. The Trump administration intends to incentivize the purchase of American-assembled vehicles through some form of tax deductibility of consumer finance payments. The details of that plan have yet to be worked out, but they would offer a significant incentive for Americans to buy American.

Speaking of missing details, the Canadian government has announced plans for a duty-remission program for Canadian vehicle manufacturers, but has not published the terms and conditions. At a minimum, we might expect that Canadian vehicle-makers might be able to be refunded any duties they pay on vehicles imported from the United States.

Canada’s applied-duty-rate advantage under the Trump tariffs increases from 2.5% to 12.5% against European and Japanese competitors; against Korean-made vehicles, it rises from 0% to 12.5%

Why impose duties on U.S.-made cars only to refund them later? By giving automakers who build cars in Canada access to duty-free imports, you are anchoring Canadian production. If production stays in Canada, manufacturers can import duty-free from the U.S. If Canadian production stops, the new counter-tariff applies. There is no impact on federal spending because the manufacturer just gets a waiver or refund of the new surcharge.

How do the numbers work out? More back-of-the-napkin math: Canadian plants produced about 1.3 million vehicles last year, with roughly 80% of Canadian production exported to the U.S. In any given year, about half of the vehicles sold in Canada are imported from the United States. Sales of new vehicles accounted for roughly 1.92 million units last year, according to Statistics Canada. So, if the normal ratios held in 2024, that would mean we imported around 960,000 vehicles from the U.S.; and exported just over a million vehicles in return. From a Canadian business perspective, manufacturers’ duty-remission savings on the Canadian side of the border would largely offset the additional cost of exporting vehicles to the United States.

By that logic, it seems jobs and investment in the automotive assembly sector are relatively secure. The tariff impact on parts companies will be partially mitigated through reduced duties on imported vehicles containing Canadian parts. In addition, the government has promised further funding to the sector which may be covered in whole or in part by any monies generated by the surcharge on U.S. parts and vehicles. So, there is reason for optimism that Canada will continue to have an auto-manufacturing sector on the other side of this dispute.

Vehicles are seen for sale at a Honda dealership in Houston, Texas, on April 7, 2025 Photo by Ronaldo Schemidt /Getty

But what about consumers? Canadian-made vehicles will experience little or no tariff impact in Canada. Imports from the U.S. under the duty-remission program for manufacturers will be duty-free, requiring no price increase. Imports from Mexico that comply with the USMCA rules of origin, even if they contain very high percentages of U.S. parts, will also remain duty-free. Vehicles imported from Europe and from Japan and Korea will be unaffected, and benefit from Canada’s existing free-trade agreements with those partners.

Only U.S.-made vehicles that are imported by companies that have no manufacturing footprint in Canada, or any U.S. vehicle that does not meet the USMCA rules of origin, will incur new costs because of the Canadian counter-tariffs.

Companies like Tesla that have no Canadian manufacturing base or can’t easily import from a third country (Tesla formerly supplied Canada with Chinese-made Models 3 and Y, until Canada put a surtax on Chinese EVs) would be hit by the new Canadian surtax. However, any company would retain the option of swapping vehicle imports to a non-U.S. source, taking advantage of lower duty rates under Canada’s other free-trade deals. So, for example, a German manufacturer might choose to supply Canada with vehicles made in Germany rather than the U.S. to avoid paying the surtax.

Workers transport Chrysler minivans at the Stellantis Windsor Assembly Plant in Windsor, Ontario, Canada, on January 31, 2025 Photo by Geoff Robins /Getty

When you put this all together, very few models will be impacted by new tariffs. I also expect that companies will plan their model lineups and consumer incentives in a way that steers consumers away from those impacted models. And, rather than delivering a 25% increase on any individual model, automakers are likely to spread price increases across their lineup in a way that minimizes consumer sticker-shock.

There will be companies and models, dealerships and workers, at the edges of this trade dispute who will be hurt, but the damage will be more contained and manageable than most people initially feared.

Tariffs will introduce new variables into the market. The new-car market in Canada last year was still smaller than it was in 2018. So, while Canada’s population has surged in recent years, it seems the rapid increase in vehicle transaction prices has kept some Canadians out of the market.

A used car for sale on a dealership lot Photo by Getty

There may be a silver lining in the tariff dark cloud. It is estimated that roughly 25% of Canadian used cars have traditionally been exported to the U.S. But since it is difficult to prove that used vehicles comply with USMCA rules of origin, tariff costs on those used-car exports will jump from 2.5% to 25% on cars and SUVs under the new automotive tariffs. Tariffs on used pickup trucks could reach 50%. As a result, fewer used vehicles will be exported.

A growing supply of used cars might allow more Canadians to get behind the wheel of new-to-them vehicles at more competitive prices. And in the new-car space, vehicles from European or Asian makers that are priced out of the U.S. market by tariffs might now find their way to Canada.

Who knows? When all is said and done, the only ones hurting from the recent U.S. tariff manoeuvres may be Americans, and you just might find a good deal if you keep a keen eye on the market and are prepared to act quickly.

Stephen Beatty: Dark clouds of auto tariffs have silver linings | driving. (n.d.). https://driving.ca/column/stephen-beatty-tariff-canada-automotive-trade-advantage-impact

This should result in an increase in used-vehicle pricing.

J.D. Power projects $6,000 price hikes on new vehicles under proposed U.S.-Canada tariffs.

Surveys show nearly half of Canadian buyers would rethink purchases if tariffs take hold.

Used-car market already sees rising demand and prices as tariffs drive consumers from new market.

The United States’s proposed tariffs are expected to raise new-vehicle prices in Canada by as much as $6,000 (some say as much as $12,000). This could prompt a shift in consumer behaviour regarding the used-car market.

Robert Karwel, director of customer success at J.D. Power Canada, said the combined effect of a 25% U.S. tariff on Canadian vehicles and reciprocal Canadian measures could lift average new-vehicle transaction prices from $49,000 to $55,000 in 2025. Karwel estimates that consumers will absorb roughly half of the additional cost, with automakers and supply chain actors taking on the remainder.

Vehicles assembled in North America, particularly those built in Canada with U.S.-sourced parts, are expected to be more heavily affected by tariff-related cost increases than models imported from overseas. Karwel said automakers are expected to maintain model price hierarchies despite the variable impact on manufacturing, likely resulting in broad price increases across vehicle lineups.

Karwel added that automakers are anticipated to reduce purchase incentives rather than raise sticker prices directly as a less visible method of cost recovery.

Consumer data indicates a potential slowdown in new vehicle deliveries created by consumers modifying their new car pans. A February 2025 survey by AutoTrader found that 47 % of Canadians planning to buy a vehicle would alter their decision in response to tariffs. Of those, 30 % said they would opt for aused vehicle instead of a new one, while 36 % reported they would reduce their overall budget.

Inventories and Used-Vehicle Market Begin to Adjust

Canadian dealers and automakers are taking steps to mitigate potential impacts. Some franchised dealerships have built up new-vehicle inventory, while manufacturers have been stockpiling units near the Canada-U.S. border. Daniel Ross of Canadian Black Book said automakers have even acquired facilities near the border to expedite logistics during trade disruptions.

Despite these efforts, industry experts expect a delayed but eventual tightening of new-vehicle inventories should tariffs remain in effect. AutoTrader vice-president Baris Akyurek said production planning adjustments will only occur if tariffs persist beyond three months. In the meantime, new car prices are expected to rise regardless of supply levels.

The used vehicle market is already experiencing a surge in demand. Prices are rising in anticipation of higher new-vehicle costs, and some consumers are accelerating purchases to avoid future tariffs. Akyurek likened the trend to the post-pandemic period, when microchip shortages led to spikes in used-vehicle values.

Export activity from Canadian used inventory is also expected to decline, according to Automotive News. U.S. buyers account for approximately 15 % of used-car exports from Canada, down from 20 % during the pandemic’s peak. Ross said tariffs will dampen cross-border demand but not eliminate it entirely due to the relatively weak Canadian dollar.

Tariffs Catch Individual Buyers Off-Guard

Beyond the broader market implications, individual consumers are also being impacted. Pat Fletcher, a 77-year-old car enthusiast from Winnipeg, faced a $46,636 bill after attempting to import a 1968 Dodge Charger RT he purchased in Texas for US$98,000. Border officials told Fletcher that the vehicle was subject to a 25 % surtax under Canada’s tariff rules.

Fletcher, as reported by CTV, said he researched applicable tariffs before purchasing but found no mention of vintage vehicles. The Canada Border Services Agency (BBSA) later confirmed that under the Customs Tariff Act, older vehicles, such as the 1968 model, are covered by a customs notice that includes items manufactured more than 25 years ago.

St-Pierre, M. (2025, March 24). Canadian new-vehicle prices may rise $6,000 amid tariff threat, pushing buyers to used market. Motor Illustrated. https://motorillustrated.com/canadian-new-vehicle-prices-may-rise-6000-amid-tariff-threat-pushing-buyers-to-used-market/150513/

Vehicles for sale at a Windsor car dealership this month. Photo by DAN JANISSE/Postmedia

There are many uncertainties about how United States President Donald Trump’s tariffs will affect the auto industry, but sector insiders say one thing is all but certain: the price to buy a vehicle is about to go up and may already be rising.

“The first economic effect we’ll see, and it’s a major one, is on car prices,” Charles Bernard, lead economist at the Canadian Automobile Dealers Association, said. “And our car prices aren’t necessarily cheap right now at the moment, so it won’t help something that was already a problem.”

It all comes as a gut punch to some who believed the auto industry was just returning to a healthy state.

The auto sector had been hit hard by inflation, with the average price of a new car in Canada rising 43.2 per cent between 2019 and 2025, and used car prices rose 39.5 per cent during the same timeframe, according to data from AutoTrader.com Inc., the vehicle marketplace. But in 2024, the average used car price declined by 12.1 per cent.

Exactly how much car prices could rise again thanks to the latest tariffs is difficult to predict. J.D. Power earlier this month estimated that 25 per cent U.S. tariffs and counter-tariffs could add $6,000 to the price of a new vehicle, which is a 9.2 per cent increase given that the average new vehicle in Canada costs $64,600, according to Autotrader.

But nearly everyone agrees that estimate is only a rough guess and there are many factors at play.

Just two months into office, the Trump administration has unleashed a barrage of tariffs, threatened tariffs and reprieves that even economists are having a hard time keeping track of, let alone making sense of their combined impacts on the auto sector.

At the beginning of March, the U.S. enacted 25 per cent tariffs on all Canadian goods that are not compliant with the Canada-United-States-Mexico Agreement (CUSMA), which could affect some auto parts manufactured here, though most vehicles are believed to be compliant. It also levied 25 per cent tariffs on Canadian steel and aluminum, both of which are large inputs for vehicles.

Trump has further signalled that he plans to enact 25 per cent tariffs on April 2 on autos and additional 25 per cent “reciprocal“ tariffs on a sweeping set of goods, which would in effect match any costs that U.S. exporters face, such as goods and services taxes, that are not generally considered as trade duties.

Analysts at S&P Global Mobility are predicting a 50 per cent probability of there being “an extended disruption” — one that lasts 16 weeks to 20 weeks — when vehicles that are more exposed to tariffs will slow or cease production.

“Consumers will face rising costs on all goods, reducing available funds and willingness and ability for purchasing durable goods,” Stephanie Brinley, associate director of autoIntelligence at S&P, said in a note on March 12. “We expect product development delays to have lasting effects into future years.”

She said one “more dire scenario,” in which tariffs on vehicles produced in Canada and Mexico are integrated into the long-term trade structure on a permanent basis, has a 20 per cent probability of happening. Although this could increase U.S. manufacturing, she said it would increase costs and likely lead to a decline in vehicle sales.

Brinley gives a 30 per cent probability for a “quick resolution” and tariffs disappearing in a month or less, but this would still lead to lower production due to supply chain issues and border gridlock.

Eventually, many economists say the tariffs could lead to inflation or a recession, which will affect interest rates and consumer behaviour, including whether to purchase a vehicle.

“With these tariffs in place, we would expect to see vehicle sales in these countries contract substantially,” Andrew Foran, an economist at TD Economics, said in a Jan. 28 note.

Even 10 per cent tariffs could lead to a sales decline of light vehicles in Canada of around eight per cent, while a 25 per cent tariff could push the decline to around 13 per cent, he said.

Since tariffs raise prices for consumers and businesses, people will have less money to spend and economic growth will weaken, Foran said. That leads to higher unemployment and stagflation, which is weak growth and high inflation combined.

“We were so close to normalcy,” Baris Akyurek, vice-president of insights and intelligence at AutoTrader, said. “Everything was coming down, the demand was there, the supply was there, we were really close to normalcy and then this stuff happened.”

He said used car prices are an important indicator because it’s the marketplace that absorbs demand when new car prices rise.

Typically, he said, used car prices start the year high and then decline, but used car prices have risen 0.4 per cent so far in March.

“It’s not by much yet, and it’s only 16 days of data, so this is not conclusive, but prices had been coming down,” Akyurek said.

On the other hand, the average price of a new vehicle declined by 0.2 per cent.

But he said there are other troubling signs in the marketplace. Sellers have stopped dropping their prices as often this year, with a 22 per cent year-over-year decline in the number of price drops amongst all vehicles listed on AutoTrader.

Some dealerships in Canada are building up inventory now, which will provide a cushion against price increases for a period of time since those vehicles will not be affected by tariffs if they are imported before they go into effect.

“It’s pretty clear what’s going on,” said Akyruek, who added that rises in price at this point “are inevitable.”

Auto prices already rising as tariffs loom | financial post. (n.d.). https://financialpost.com/transportation/autos/auto-prices-already-rising-tariffs-loom

Used vehicles for sale are displayed at an automotive dealership in Ottawa on Friday, Aug. 11, 2023. THE CANADIAN PRESS/Sean Kilpatrick

Thanks to the trade war, your next vehicle could be used.

Even then, the savings might not be what you expect.

As indiscriminate U.S. tariffs threaten to shut down the North American auto industry, manufacturers of new cars will be the first to be hit. That’s expected to drive more buyers to the used-car market, complicating what many already find to be a fraught spending decision.

New car economics: The Michigan consultancy Anderson Economic Groupestimated that new car prices could go up by US$12,000 if the U.S. implements 25 per cent tariffs on Canada and Mexico and an additional 10 per cent on China. That’s because many car parts would be tariffed multiple times before they ended up in assembled vehicles. What’s more, some suppliers and car plants may slow or halt production because they’re unable to pay the costs, reducing the supply of vehicles over time.

“No matter how much the tariff will be, it is not possible to move production back to the U.S. overnight. So most likely, either production will have to shut down, or they have to continue under tariffs and be hit,” said Tu Nguyen, an economist at the tax and consulting firm RSM Canada.

Either way, prices of new cars go up.

Used car economics: As of this writing, it wasn’t clear whether used cars would fall under the U.S. tariffs. But a recent analysis by the Canadian Black Bookfound that, either way, Canadians will gravitate to second-hand vehicles.

If used cars are tariffed when crossing the border, the price gap between new and second-hand ones will widen. That’s because fewer U.S. buyers would be bidding at Canadian car auctions due to the additional expense of bringing cars across the border. Canadians would have more used vehicles to choose from.

That’s a happy scenario for buyers, but there are others in the Black Book analysis where used car prices rise. In one, Canadians react to higher new-vehicle prices by migrating en masse to the pre-owned market, and demand eclipses supply. In another, the tariffs don’t apply to second-hand autos, prompting American bidders to snap up used Canadian vehicles at favourable exchange rates, driving up prices at auctions.

“Used cars—[that] is the question mark in terms of what will happen,” said Jesus Ballesteros, who advises manufacturers and other businesses as a partner at BDO Canada. Regardless, dealers are turning to second-hand cars as a revenue stream. To the extent that dealers can prepare at all, Ballesteros said, having “a good used car operation” will dampen the impact of tariffs.

Chaos at the dealership: Tariffs aren’t yet in effect, but dealers are already planning for the ensuing chaos. For starters, they’re on high alert for fraud. Insurance company Aviva expects a tighter U.S.-Canadian border to increase the probability that Canadians accidentally buy stolen vehicles, because thieves will flip them domestically rather than risk trying to get them into the U.S.. Among the other unknowns: how a trade war will affect interest rates; the costs of repairs using tariffed parts; and the economic fluctuations tariffs may cause in local markets, noted Charles Bernard, lead economist at the Canadian Automobile Dealers Association.

Sean Mactavish, CEO of Autozen, a Vancouver-based tech company that helps car owners sell to dealerships, is among those expecting a surge in demand for second-hand vehicles. How the prices shake out depends on how long people delay purchases amid economic uncertainty, he noted. He’d like to see governments quickly lift interprovincial trade barriers for car sales to make it easier for dealers to find the vehicles and workers they need within Canada.

In the meantime, Mactavish is navigating the same unknowns as everyone. How great will the impacts be? Which market segments will get hit hardest? “I’ve talked to other leaders and dealerships, and we’re all asking the same questions,” he said, “trying to get answers.”

Balakrishnan, A. (2025, March 13). Why even used cars could get more expensive in a trade war. The Logic. https://thelogic.co/news/shift/used-cars-auto-tariff-trade-war/

There could be trouble brewing in the Canadian wholesale used-vehicle market.

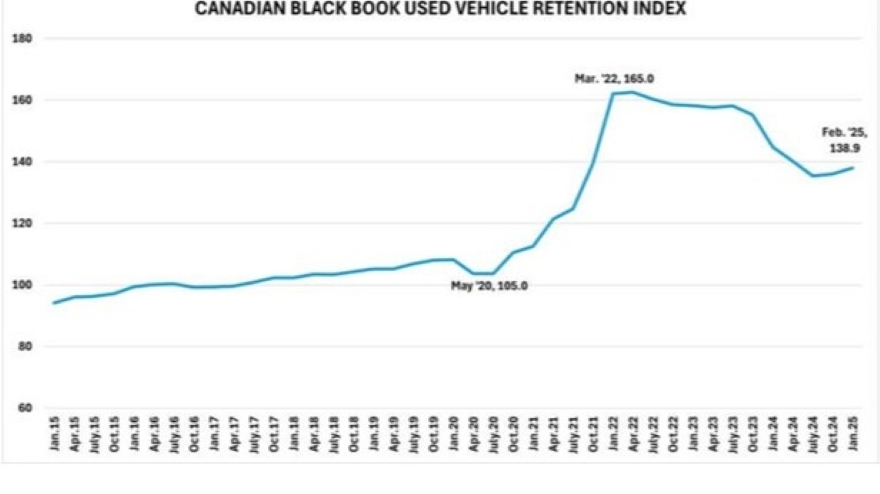

Canadian Black Book’s Used Vehicle Retention Index rose 0.9 points to 138.9 in February. It wasn’t the eye-opening 2.3-point jump of the previous month, and was still down 3.3% year-over-year, but CBB senior manager and head of Canadian vehicle valuations David Robins said it’s part of an upward trend that will continue to be fueled by the U.S. government’s 25% tariff on Canadian imports and Canada’s reprisal.

“Wholesale vehicles values in Canada are under upward price pressure in February with volumes decreasing and demand staying strong,” Robins said. “As U.S. tariffs have been implemented on March 4 and a Canadian retaliatory response is being phased in over the following 21 days, we expect increased instability while markets adjust to these major changes.”

President Trump’s announcement Wednesday of a one-month tariff exemption for autos complicates that assessment as the market reacts to the new circumstances. Trump’s “reciprocal tariffs” are scheduled to take effect April 2.

Until January’s sudden rise, the CBB index had been steady through the second half of 2024, gaining or losing less than 0.6 points during any month in that period. Prior to that, the index spent 27 months dropping as the market corrected from a COVID-induced peak of 165 in March 2022.

The index is calculated using CBB’s published wholesale average value on 2-6-year-old used vehicles as a percentage of original typically equipped MSRP and weighted based on registration volume and adjusted for seasonality, vehicle age, mileage and condition.

Big week for auction sales

CBB’s weekly Market Insights report said the biggest change in the wholesale landscape for the week ending March 1 showed up in the auctions, where sale rates rose to an average of 54.3%, up five percentage points from the previous week, with a range from 52.6% to 76.1%.

Overall values fell 0.19% for the week, slightly less than week before, with three segments gaining — compact vans (up 0.02%, $3), full-size pickups (0.29%, $96) and sub-compact cars (0.25%. $29) — gaining and sporty cars breaking even.

On the downside, six segments lost more than $100 in value, topped by full-size crossover/SUVs ($402, 0.66%) and prestige luxury cars ($272, 0.46%).

Used retail prices held steady week over week, with the 14-day moving average listing price remaining at $34,000.

CBB analysts noted a record 18.9% market share for zero-emission vehicles in the fourth quarter of 2024 as consumers raced to buy in front of the pending end of ZEV decrease/end of various rebate programs from federal and provincial governments, leading to a record 15.4% share for the year. Both of those numbers were up 40% year-over-year.

Not surprisingly, ZEV market share fell in January to 13.3%, which was still a 2.9% increase from January 2024.

The U.S. market was a mirror of the previous week with values down 0.19% overall, cars down 0.25% and trucks dropping 0.16%. Analysts said early indications of rising prices in select segments could be the harbinger of a spring market, as the overall decline remained less severe than the typical seasonal declines.

CBB’s 2025 forecast tells industry ability to pivot is key in a “tumultuous” year. Auto Remarketing. (n.d.). https://www.autoremarketing.com/arcanada/cbbs-2025-forecast-tells-industry-ability-to-pivot-is-key-in-a-tumultuous-year/

Stability reigns in the Canadian wholesale used-vehicle market.

While the threat of tariffs and a trade war with the U.S. loom on the horizon, the week ending Feb. 22 looked a lot like the previous few: a mild downward drift of 0.22% overall and solid auction sales rates, according to Canadian Black Book’s weekly Market Insights.

The pace of the decline did pick up a bit after losses of less than 0.20% in six of the past seven weeks, with truck/SUV segment values down 0.21% and cars dropping 0.23%.

Compact vans took the largest percentage fall at 0.95% ($184), followed in the truck/SUV category by mid-size crossover/SUVs (0.60%, $225), small pickups (0.49%, $135) and sub-compact luxury crossovers (0.45%, $96).

Among cars, full-size cars were down 0.66% ($133), sub-compact cars dropped 0.55% ($54) and compact cars fell 0.42% ($58). Prestige luxury cars ($232, 0.40%) and premium sporty cars ($159, 0.20%) took the biggest dollar losses.

Only two segments gained value for the week: mid-size crossover/SUVs (up 0.29%, $69) and compact crossover/SUVs (0.11%, $19).

Monitored auction sale rates were steady, averaging 49.3% with a range from 39.5% to 70.1%, and retail prices continued to sink, with the 14-day moving average retail listing price for used vehicles down to $34,000.

The U.S. market remained on course, showing the expected seasonal behavior. Late-model vehicles aged 0-to-2 years neared positive territory after a minimal decline of 0.08% for the week, and high-volume segments like compact cars (up 0.02%) and compact crossovers (up 0.002%) recorded small gains. The overall market was down 0.19%.

Canadian Wholesale Market Stable as tariffs loom. Auto Remarketing. (n.d.). https://www.autoremarketing.com/arcanada/canadian-wholesale-market-stable-as-tariffs-loom/