Dealers are having to shift as used car prices decline and borrowing costs remain elevated.

Anomaly is perhaps the best way to describe what happened to the used vehicle market between 2020 and 2023. The COVID-19 pandemic and resulting lockdowns caused OEMs and their suppliers to curtail production. For dealers, this had several implications. Firstly, it reduced the availability of new vehicles for a few years. Secondly, it put pressure on lease returns and used vehicles. Plus, with public transit ridership falling off a cliff due to social distancing requirements, a whole host of new vehicle shoppers entered the market.

The result? Rising vehicle demand and with it, transactional prices. In fact, prices became so elevated that in many cases, three and four-year-old vehicles were commanding more money than they did when new. Dealers frequently found themselves scrambling for used inventory and when they were able to get it, turned record profits for each unit sold, resulting in a seller’s market the likes which have not been seen since the days following World War II—a time when the public was literally starved for cars.

Elevated costs

Since 2022 however, the market has shifted yet again. Rising inflation and the Bank of Canada’s aggressive interest rate hikes put pressure on both dealers and consumers. Today, we’re faced with a situation where prices for used vehicles remain elevated, but new car inventory is improving. This means that dealers are having to adjust their approach to used car operations yet again.

According to Daniel Ross, Senior Manager, Industry Insights & Residual Value Strategy, at Canadian Black Book, with used vehicle inventories improving in the U.S., there has been less interest in shipping cars across the border. From a peak of 374,000 units crossing from Canada to the U.S. in 2021, that demand has consistently declined, easing used vehicle demand here at home and facilitating price declines. As a result, we’ve seen lower retail pricing and an increase in the number of days to turn inventory, as dealers look to maintain buyer interest and shift metal off their lots.

Below pre-pandemic levels

Jeff Schulz, Executive Vice President, Marketing at LGM Financial Services, notes that while the availability of used vehicles has improved, it’s still significantly below pre-pandemic levels. Plus, with the overall economy slowing and interest rates remaining elevated, many consumers are scaling back on big-ticket purchases, including vehicles.

This means dealers will often need to be creative when it comes to moving used inventory. “It’s important for dealers to understand their local market,” says Schulz. “You need to know what kinds of vehicles are in demand and do your best to cater to that customer base.” In B.C.’s lower Mainland, for example, Schulz notes that fuel efficiency is currently a top priority for many consumers, so focusing on fuel-efficient vehicles and those that are likely to appeal to a more environmentally conscious buyer such as hybrids and PHEVs likely make more sense. In other markets, small SUVs and pickups might be in high demand, so it’s important for dealers to understand what is selling and what isn’t and prioritize sourcing their used inventory accordingly.

Higher payments

At AutoTrader, Baris Akyurek, Vice President, Insights and Intelligence, notes that the firm’s data points to a 2.1% year-over-year decline in used vehicle prices, yet at the same time, the cost to finance those vehicles has increased. For consumers, Akyurek notes that in February 2019, it cost $450 per month to finance the average used vehicle. By February 2024, that had increased by 36.5% to $636. Additionally, affordability issues are stretching loan terms—with the average duration increasing from almost 68 to over 72 months between February 2019 and 2024.

Additionally, for dealers, floor plan financing is significantly more expensive today, so, as Daniel Ross at Canadian Black Book notes, finding the right vehicles that can be quickly turned is far more critical now than even a couple of years ago, meaning that dealers need to focus on more efficient remarketing efforts and should not be tempted to hold out for the “right” buyer. “The repercussions of keeping inventory too long or holding out on price for that right buyer highly expose consistent profitability,” he says. “Stick to the process enforced at the dealership and improve upon areas that slow things down.”

F&I considerations

According to Jeff Schulz, dealers can satisfy both consumer demand and improve inventory turn by creating solid F&I packages for their used vehicle customers. Given that pricing is still expensive, as are financing rates, with many consumers looking to stretch the loan terms to improve affordability, anything to address consumer peace of mind when it comes to a used vehicle purchase is paramount. That’s why Schulz says that certified pre-owned programs are proving particularly popular, demonstrating that the vehicle has gone through a rigorous, multi-point inspection program prior to being certified for sale.

Additionally, Schulz notes that loan protection can be a good option since it can provide assurance in the advent of disability or job loss, especially as the economy continues to slow. Extended warranties can also make a significant difference. “Used vehicles tend to have higher rates of mechanical failure, so an extended warranty provides added assurance to the customers,” Schulz explains. “Furthermore,” he says, “they can also serve as a retention tool, bringing the customer back to the dealer for service and eventually their next vehicle.”

Evans, H. (2024, March 20). Used vehicles: Navigating through a changing market. Autosphere. https://autosphere.ca/dealerships/2024/03/19/used-vehicles-navigating-through-a-changing-market/

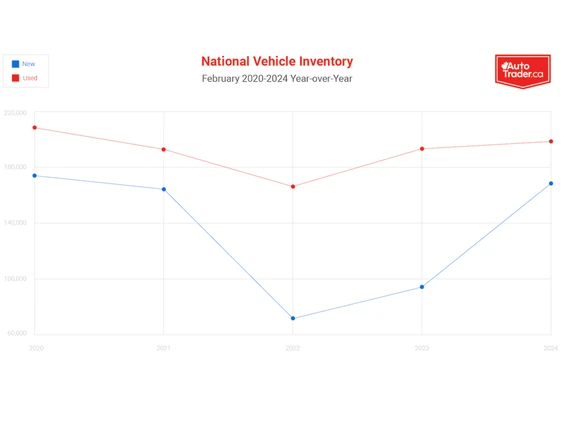

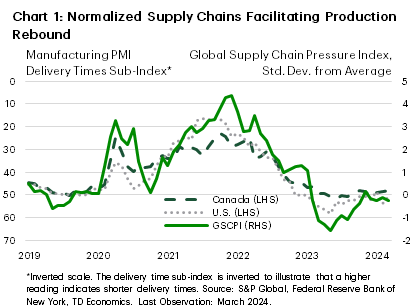

The automotive industry returned to a state of normality in 2023 as easing supply chain issues improved procurement times (Chart 1) and facilitated a rebound in production. As a result, North American light vehicle production increased 9.6% last year, putting total production only 3.9% below 2019 levels. This helped to push inventory levels to their highest level in three years to start 2024.

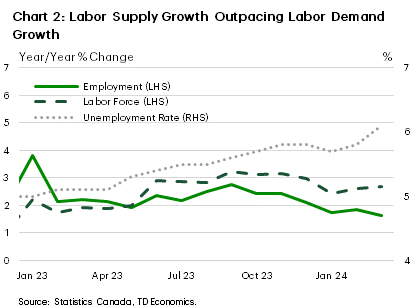

The automotive industry returned to a state of normality in 2023 as easing supply chain issues improved procurement times (Chart 1) and facilitated a rebound in production. As a result, North American light vehicle production increased 9.6% last year, putting total production only 3.9% below 2019 levels. This helped to push inventory levels to their highest level in three years to start 2024. The Canadian labor market is not quite as weak as is suggested by the one percentage-point increase in the unemployment rate over the past year. With the nation’s population growing by 3.2% last year, we have seen labor force growth outpace employment growth consistently since May 2023 (Chart 2), which has exerted upward pressure on the unemployment rate. Canadian job gains in 2023 actually exceeded those seen in 2019 by more than 100k jobs, but the economy would have needed roughly 160k additional new jobs to offset outsized labor force growth and keep the unemployment rate unchanged relative to the start of 2023. At the same time, while part-time jobs contributed more to last year’s gains than usual (25% vs. 3% in 2019), full-time job growth was above that seen in 2019. So, while the Canadian labor market is not remarkably strong, it is not currently in the doldrums either.

The Canadian labor market is not quite as weak as is suggested by the one percentage-point increase in the unemployment rate over the past year. With the nation’s population growing by 3.2% last year, we have seen labor force growth outpace employment growth consistently since May 2023 (Chart 2), which has exerted upward pressure on the unemployment rate. Canadian job gains in 2023 actually exceeded those seen in 2019 by more than 100k jobs, but the economy would have needed roughly 160k additional new jobs to offset outsized labor force growth and keep the unemployment rate unchanged relative to the start of 2023. At the same time, while part-time jobs contributed more to last year’s gains than usual (25% vs. 3% in 2019), full-time job growth was above that seen in 2019. So, while the Canadian labor market is not remarkably strong, it is not currently in the doldrums either.

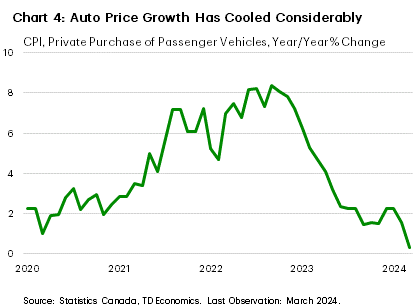

The first reason is owing to the delayed post-pandemic recovery in the automotive sector. The lack of available inventory in the market over the past three years has created a build-up of pent-up demand, which is one of the reasons why Canadian vehicle sales growth roughly matched that seen in the U.S. last year despite materially different economic trends. As production ramped up and supply levels gradually improved last year, consumers in both countries pushed sales to their highest level since 2019. This is expected to continue to support sales moving forward, with moderating vehicle prices (Chart 4) and lower financing costs providing support to this channel through the second half of the year.

The first reason is owing to the delayed post-pandemic recovery in the automotive sector. The lack of available inventory in the market over the past three years has created a build-up of pent-up demand, which is one of the reasons why Canadian vehicle sales growth roughly matched that seen in the U.S. last year despite materially different economic trends. As production ramped up and supply levels gradually improved last year, consumers in both countries pushed sales to their highest level since 2019. This is expected to continue to support sales moving forward, with moderating vehicle prices (Chart 4) and lower financing costs providing support to this channel through the second half of the year.