Canadians are used to hearing about pricey housing. But another expense has quietly grown to mortgage-sized proportions for many: their car.

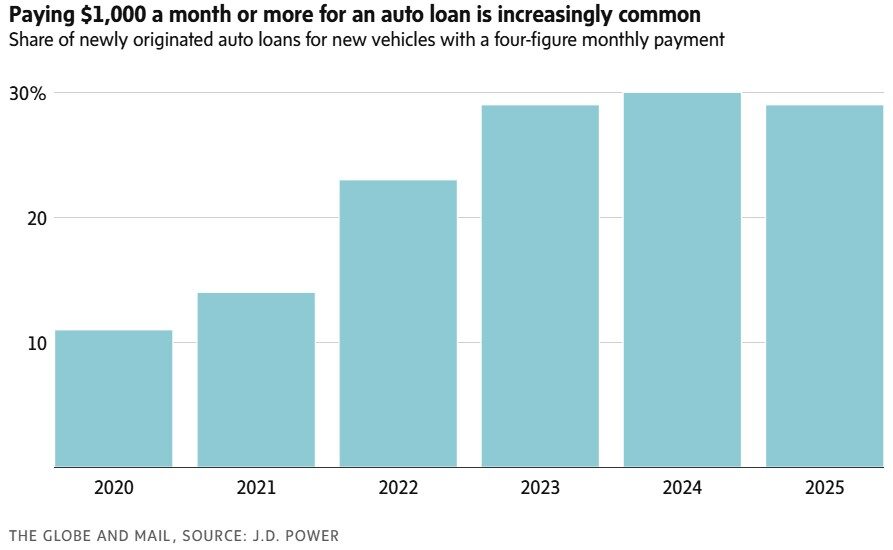

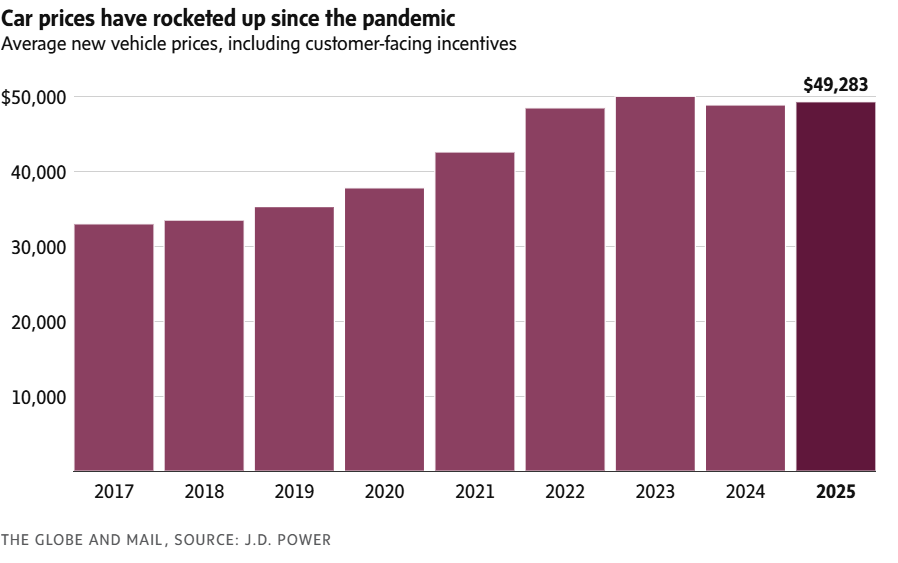

With consumers now paying around an average of $50,000 for a new ride, nearly 30 per cent of auto loans in the new-vehicle market come with a monthly payment of $1,000 or more, according to analytics firm J.D. Power. It’s a similar story in the lease market, where the average payment is just under $800 a month.

For comparison, the average price of a new vehicle was $12,000 in 1985, according to Statistics Canada, equivalent to just over $31,000 in 2025, adjusted for inflation. That’s below what the average second-hand car costs today.

Meanwhile across both the new- and used-vehicle markets, the most popular auto loan term length has grown to seven years, the J.D. Power data show, as Canadians stretch out amortizations to keep monthly payments manageable.

Ever more sophisticated technology, government regulations, the push toward electric vehicles, pandemic disruptions and, lately, auto tariffs all help explain why cars have become so expensive.

As auto companies retreat from Canada, do government subsidies still make sense?

Opinion: Trump is turning America’s auto industry into a global backwater. Canada must now go its own way

But the end result for consumers is the same: Car payments are increasingly like mortgages. That’s not just because of their size in dollar terms, but also because, just as housing costs, they take up a massive portion of household budgets.

The after-tax income of a typical Canadian household 40 years ago was around $62,000 in inflation-adjusted terms, according to Statscan. In 2023, the latest available data, it stood at $74,200, or around $77,000 in 2025 dollars. That’s a 24-per-cent rise in real terms.

That may seem a healthy increase (although much of that growth comes from government transfers, rather than wage gains). But it pales compared with the trajectory of car prices, which jumped by around 70 per cent over the same period.

Buying a second-hand vehicle is an obvious way to keep car payments in check. But even that is hardly a bargain. For the past four years, average prices have been firmly above $35,000, according to J.D. Power.

In smaller cities where housing remains affordable, the gap between mortgage and auto loan payments has become alarmingly small. In Saguenay, Que., for example, the average mortgage instalment is $886 a month, only around $340 more than the typical monthly auto loan charge of $547, according to data from Equifax and the Canada Mortgage and Housing Corp.